Show Me The MONY

Stock deep dive - MONY Plc

(Disclosure : I own shares in MONY plc)

Risk rating : Balanced

Stock style : Contrarian

Business Overview

MONY Group is a multi-product price comparison website (PCW), operating a common tech platform across three key consumer brands– Moneysupermarket, MoneySavingExpert and Quidco. It operates a two-sided digital marketplace, connecting consumers seeking to reduce household bills with service providers (insurers, lenders, utilities) in exchange for a click-through or referral fee. Unlike other PCWs who have their roots in car insurance, MONY (as the name suggests) has a broader offering, particularly in finance. In addition they have a small but fast growing B2B white label business.

Key Historic Events

• MONY was founded by Simon Nixon and Duncan Cameron in 1987 and Moneysupermarket.com launched in 1999, rapidly expanding from mortgages into credit cards, loans, insurance (2003), travel (2004), and utilities.

• The IPO in June 2007 valued the business at circa £1 billion.

• 2012: Acquisition of MoneySavingExpert.com from Martin Lewis for £87 million. This gave MONY access to an editorially independent, highly trusted consumer finance media brand.

• 2017-2019: Peak profitability. The group reached an all-time high share price of ~400p , reflecting the maturing of the insurance comparison market and strong pricing power.

• 2020-2021: COVID-19 headwinds. Travel collapsed, energy switching was disrupted, and the lockdown effect suppressed motor insurance switching (fewer cars on the road = fewer renewals). Profits fell ~40%.

• 2021: Acquisition of Quidco for up £97m. A strategic bet on cashback as an adjacent model to retain consumers between annual insurance cycles. Execution has been mixed, diluting group margins – so far a poor acquisition ?

• 2024: Rebrand from Moneysupermarket.com Group plc to MONY Group plc

• 2024-2025: SuperSaveClub launch and scaling. This is the key strategic initiative of the current management — a membership model designed to build direct customer relationships, reduce PPC cost reliance, and increase CLTV. Currently 2.1m customers registered - target is >3m

• 2025-2026: Strategic partnership with OpenAI / ChatGPT, launch of Price Optimiser and Savings by MoneySuperMarket, deconsolidation of Ice Travel Group.

Divisional Structure & Revenue Growth

Divisional Structure

• Insurance (52% of FY2025 revenue, £233m, growth -1%): Car, home, travel, life and pet insurance comparison. This is the highest-margin vertical (EBITDA margin ~60-65%) and the group’s largest earnings driver. Revenue is correlated with the level of premium inflation in the market — when premiums rise, consumers shop more aggressively as we saw in 2024, a strong year for this division with revenues up 7%. By contrast 2025 was muted as premiums fell,

• Money (24% of revenue, £105m, growth +8% ): Credit cards, loans, mortgages, savings. Driven by interest rate cycles — falling rates should stimulate mortgage and credit card switching but compress savings product attractiveness. The MoneySavings Expert brand is highly visible in the UK with over 9m newsletter subscribers and benefits from the extensive media profile of founder Martin Lewis.

• Home Services (11% of revenue, £48m, growth +33%): Broadband, mobile, and energy switching. Energy switching was suspended by Ofgem during 2021-2024 given market dislocation; the restart of switching was a meaningful tailwind in 2025, with Home Services revenue up 33% from a fairly low base.

• Cashback/Quidco (12% of revenue, £53m, growth -13%): Lower-margin business (EBITDA margin ~13%) acquired for £97m late 2021. Provides customer acquisition at lower cost but dilutes group-level profitability. A strategic ?

• Travel: (4% of revenue, £18m, growth -10%): Structurally subscale post-pandemic. Now a minority position at 49% and largely irrelevant going forward.

• B2B / Decision Tech: White-label comparison technology for third-party brands. Now live with 35 partners across car, home, broadband, mobile and energy including Auto Trader and Rightmove. Not separately disclosed but revenue up 49% in FY2024 from a very low base. A nascent but potentially helpful growth engine.

Revenue Growth

Revenue growth has been volume-led in recent years, with pricing power fluctuating by vertical. The strategic ambition is to shift mix toward higher-CLTV membership revenue (SuperSaveClub), B2B platform fees, and adjacent financial product categories (savings, investments) where MONY has competitive advantage over other PCWs.

Revenue is predominantly performance-based: providers pay a cost-per-acquisition (CPA) or click fee when a consumer converts. This aligns incentives and makes the revenue model inherently correlated to consumer switching activity, not simply traffic. The model is highly scalable given the shared tech platform, which explains the high incremental margins. Active user numbers reduced by 1.1m to 12.7m in 2025, primarily driven by reduced car insurance enquiries as the market contracted. However,revenue per active user grew by £1.67 to £20.21, supported by increased levels of energy switching, stronger revenue and sales in life insurance, and increased activity across borrowing channels

Key current growth drivers include :

• SuperSaveClub Scaling: Currently 2.1 million members generating 16% of group revenue. The suggestion is that 3-4m members are possible. If CLTV is genuinely 2x that of non-members, each incremental million members at £35 ARPU implies £35m of incremental high-quality revenue.

• Energy Switching Restart (Home Services): Home Services revenue jumped 33% in FY2025. The reopening of the energy switching market after Ofgem restrictions is a multi-year structural tailwind. Pricing normalisation in energy markets has also increased consumer motivation to switch.

• Money Vertical (Interest Rate Cycle): With UK interest rates easing from cycle highs, the credit switching market (credit cards, loans) should benefit from re-stimulated demand. The mortgage switching market is a multi-year re-stocking opportunity as 5-year fixed rate deals originated at 2020-2022 lows start to mature.

• B2B/Decision Tech: 49% revenue growth in FY2024, 35 live partners. This is a scalable, capital-light revenue stream that shares the existing platform cost base. A potential re-rating catalyst if scale becomes visible.

• AI-Enabled Products: Price Optimiser (helping customers save on car insurance), Savings by MoneySuperMarket (entry into the £1 trillion+ UK savings market), and the ChatGPT app partnership. These are early-stage but reflect a credible attempt to position MONY as a participant in the AI-driven financial services journey rather than a potential disintermediation casualty.

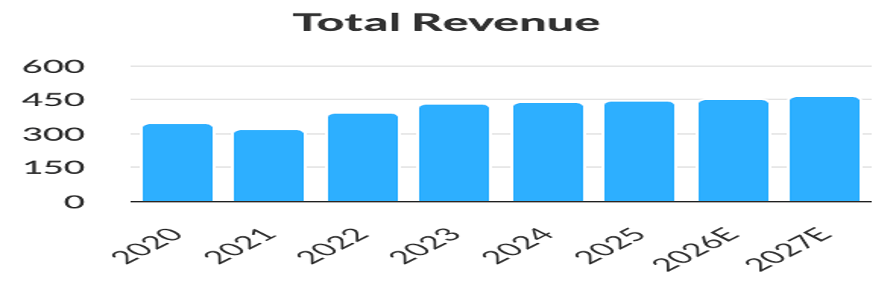

Organic revenue growth at MONY was +2% in both ’24 and ’25 and is forecast to remain modest at 2-3% CAGR underlying over the next two years (note 2026 reported is expected to be flat due to the deconsolidation of Travel)

Margins & Returns

Profit Margins

MONY is a tech and data-led digital platform. The key variable impacting it’s gross margin is marketing spend, notably Google PPC, where in 2025 there was eye-watering inflation of >20%, reflecting Google’s monopoly status. The cut-throat nature of PCWs with four players in the UK throwing money at Google makes this an ongoing problem. Marketing spend was £196m in 2025 (+6%), representing 43.6% of sales, up from 42% in 2024. Of this online spend (mainly Google) was 51%. It therefore makes sense for MONY to promote their own loyalty scheme and in-app usage as rapidly as they can. Direct traffic is currently >40% of revenues, having been as low as 24% four years ago, with the SSC now 16% of total sales from a standing start 2 years ago. They now offer loyalty customers a discount so there is a short term margin cost but in the long term a lifetime customer value benefit which will improve retention and quality of earnings. The question is how much the loyalty scheme can drive growth and improve margins from here.

• Gross margins have fallen from 68% in ’23 to 66% in ’24 and 64% in ‘25, primarily due to elevated Google PPC costs (up 21% per unit in 2025). In effect the four UK PCWs are cutting each others throats whilst enriching Google. Can Chat GPT/AI alter this balance of power in favour of MONY ?

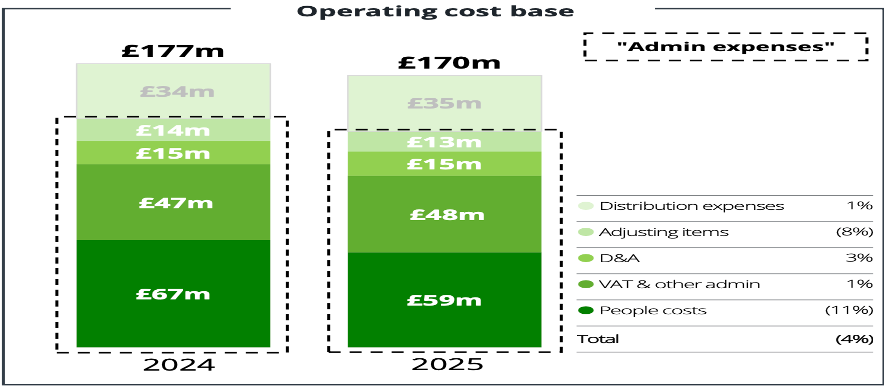

• Cost discipline: Operating expenses declined 4% in FY2025 having already fallen 9% in 2024. The cost control culture is strong here through re-engineering and efficiency initiatives, demonstrating management’s ability to offset gross margin pressure and benefit from reduced staffing costs (-11% in ’25) in the AI era. Mgmt are now guiding for relatively flat costs in ’26 ie.some low hanging fruit re people costs has already been picked

• EBITDA margins continue to increase as a result of reduced costs - 31% in ’23 to 32% in ’24 and 33% in ’25 - still a pretty healthy measure in absolute terms (they have ranged from 30-36% over the past 5 years). Analyst reports suggest that this will be stable/flat from here, but clearly disintermediation threats from AI sources could materially reduce this in a worst case scenario.

• Operating margins are high as you would expect for a platform business – currently 29% - and also forecast by most analysts to remain stable.

The P&L is structured by divisional ebitda contribution margins, ranging from money & home services at around 65%, insurance at 55% and Quidco way lower at 10-20%. Everything runs from one central tech platform which allows MONY to dial up and down on verticals depending on market conditions and allows for smoother margins than if they were all stand alone businesses.

Returns

MONY’s historical ROIC peaked at circa 49% in 2019 driven by the capital-light model and strong insurance market conditions but has been on a downward trend since. It is currently estimated at 34.8% by Berenberg, still a healthy number reflecting their proprietary, scalable infrastructure that underpins all their comparison verticals and the B2B decision tech offering. This combined with 30+ years of consumer data make the platform hard to replicate quickly.

BofA Securities estimates ROIC will fall further to c.27% by 2030, reflecting higher PPC costs, Quidco dilution, and increased investment in membership infrastructure. This is the most bearish analysis currently in the market.

Industry Structure & Competition

The UK price comparison website (PCW) market for financial services is dominated by four players: Compare The Market (privately held, part of BGL Group), Go.Compare (owned by Future plc, listed), Confused.com (owned ZPG Group, private), and MoneySuperMarket. The structural dynamics are those of a high-fixed-cost, high-marketing-intensity market where brand promotion drives consumer intent. UK regulatory frameworks (FCA, Ofgem) consistently incentivise switching and prohibit discriminatory loyalty pricing. This structurally reinforces the demand for comparison services in the UK.

Essentially they are all doing similar things but MONY is the group with the greatest diversification strategy, being the only one whose roots weren’t in car insurance. Compare The Market is the clear leader in insurance with over 50% share. It’s hard to get reliable public data but the bullets below offer some context

• Compare The Market: est sales £560m - the clear market leader in insurance, powered by relentless ‘meerkat’ brand investment and a premium-skewed customer base.

• Go.Compare (Future plc): est sales £150-175m. Mainly insurance and currently a significant part of the Future market cap. Possible disposal candidate ?

• Confused.com : the smallest player , est sales £100-130m (although ZPG also owns USwitch)

• MoneySuperMarket: ’25 sales £445m. strategically differentiated through MoneySavingExpert (editorial/media), Quidco (cashback), B2B/Decision Tech and the SuperSaveClub membership model.

MONY sits between the consumer and the financial services provider — a classic aggregator or ‘demand aggregator’ role. Its economic moat derives from the fact that it controls a high-intent, cost-efficient distribution channel for products that are purchased infrequently (typically once a year for insurance). Providers cannot individually replicate the breadth of demand aggregation; consumers benefit from transparent, multi-provider comparison. This creates genuine bilateral value — but also structural tension, as providers seek to disintermediate over time.

MONY’s shift to a membership model (SuperSaveClub) is partly a response to the fact that raw CPA economics are inherently commoditised — MONY is trying to build a recurring, margin-accretive revenue stream that is less exposed to provider pricing pressure.

Cashflow, Balance Sheet & Capital Allocation

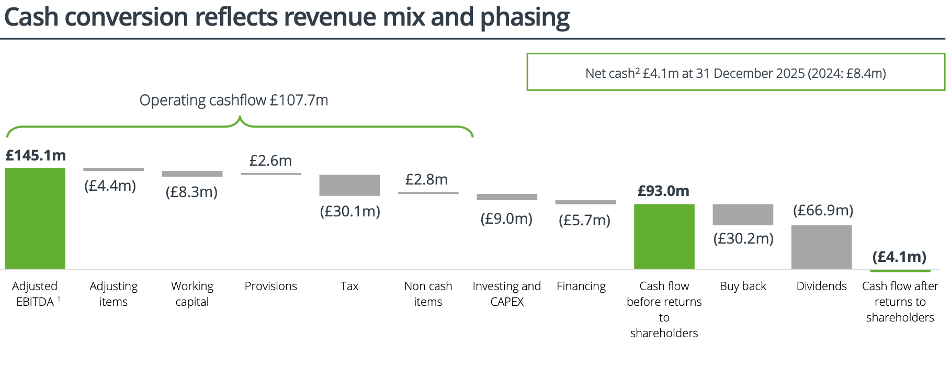

There is a small amount of net cash (£4m) and this was after a £30m SBB and £67m dividend cost in 2025. The SBB planned for ’26 is £25m whilst the dividend is set to grow only modestly if at all, with management stating a desire to improve cover from the current 1.4x. In total they plan to return £90-95m to shareholders in 2026, around 100% of FCF whilst retiring 3-4% of the equity each year, therefore reducing some of the high dividend burden here.

Operating cash flow of £108m in FY2025 was down 7% mainly due to working capital swings. These are usually not material but increased activity in energy and life assurance did have an impact in 2025 with cash conversion lower at 74% compared to >90% historically. A metric worth keeping an eye on given the slippage in 2025 and the the improved activity in these areas.

Capex has peaked and fell last year to only £9m (2% of sales, mainly tech) v £14m in ’24, reflecting the capital light nature of the model. They spent £42m on tech/product in ‘25 with the other £33m taken to the P&L – looks pretty clean. The total reinvestment rate which includes brand marketing, capex, new product development etc. was 9% of sales in ’25 v 11% in ’24 so overall investment has been falling from a previously high level. Management are not flagging any AI-related expenses from here and claim to have a fully invested and integrated platform.

M&A doesn’t appear to be a major part of the strategy going forward outwith a currently unlikely consolidation in the PCW market. The only notable deal in the recent past was the purchase of Quidco in 2021 for £97m.

Management, Governance & Shareholders

Senior Leadership

• Peter Duffy, CEO (appointed September 2020): Previously CEO of Just Eat, CCO at easyJet, and Marketing Director at Audi UK. Digital platform and marketing expertise is directly relevant. Duffy has overseen a disciplined strategic evolution — the rebrand, SSC launch, B2B platform development and AI partnership. His tenure has coincided with revenue and EBITDA growth, though the share price has substantially derated.

• Niall McBride, CFO: Has maintained strong cost discipline alongside strategic investment, most evidenced by the 4% decline in operating expenses while holding margins in FY2025. The RCF extension and conservative balance sheet management reflect prudent capital discipline.

• Jonathan Bewes, Non-Executive Chair (appointed January 2025): Chartered accountant with 25 years of investment banking experience. Also serves at SAGE plc, Next plc, and the Court of the Bank of England. Strong governance credentials.

Incentives & Governance

• Management incentivisation is linked to adjusted EBITDA and relative total shareholder return. The shift towards membership metrics (SuperSaveClub members) as an operational KPI suggests an attempt to align management behaviour with longer-duration value creation rather than simply annual profit maximisation.

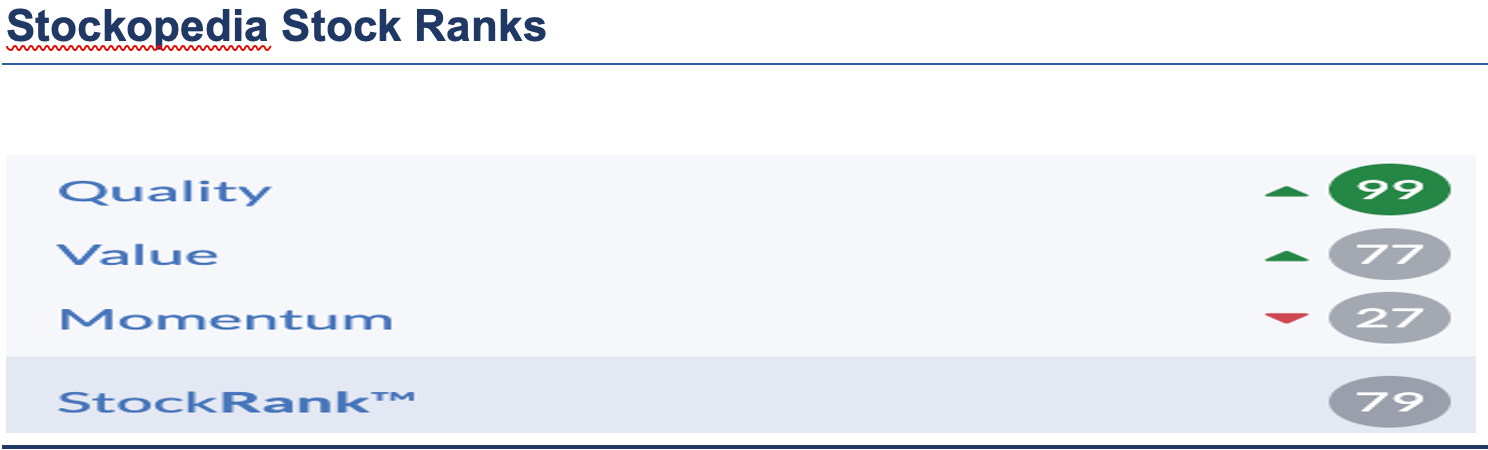

• The ISS QualityScore of 3 reflects some areas of governance scrutiny, particularly on compensation (score: 5). Investors should review remuneration report detail on LTIP vesting conditions and whether they are sufficiently stretching relative to peers

Shareholders

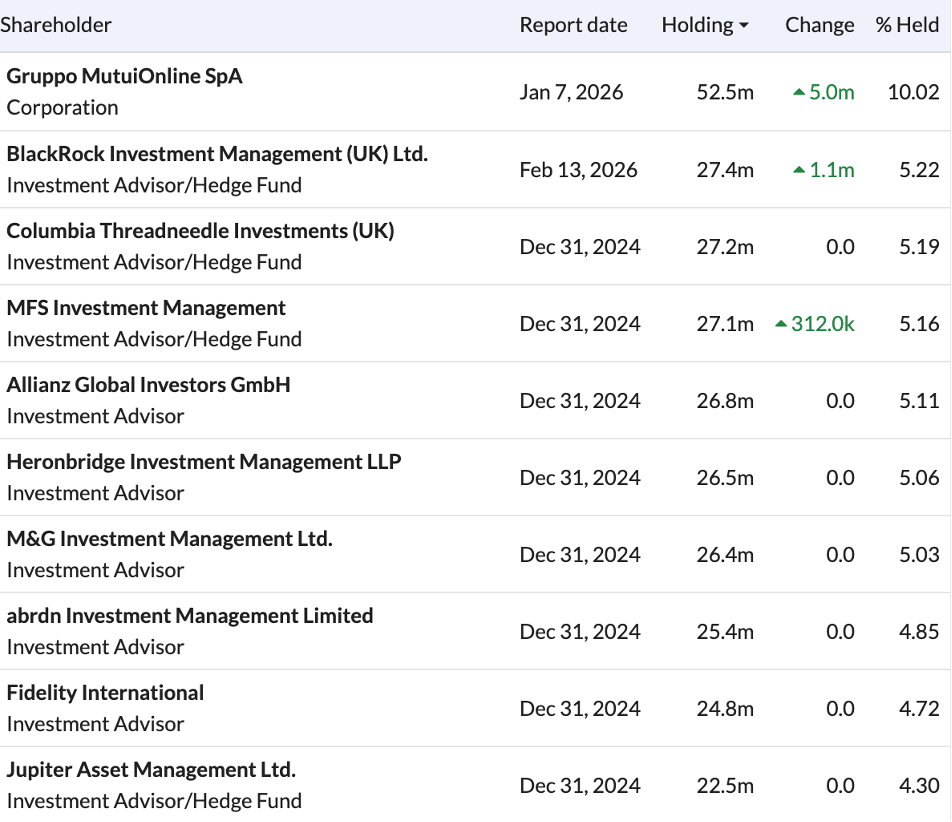

Management - Exec management don’t own many shares despite recent falls, which is a real red flag IMO. CEO got a total package of £2.5m in ’24 but only owns around £600k of equity. Note £20k purchase from an NED post results this week.

Other shareholders - interesting stake of 10.0% held by an Italian PCW player, Gruppo MutuiOnline, which they have built up since 2022. Other than that it’s a fairly mainstream institutional list.

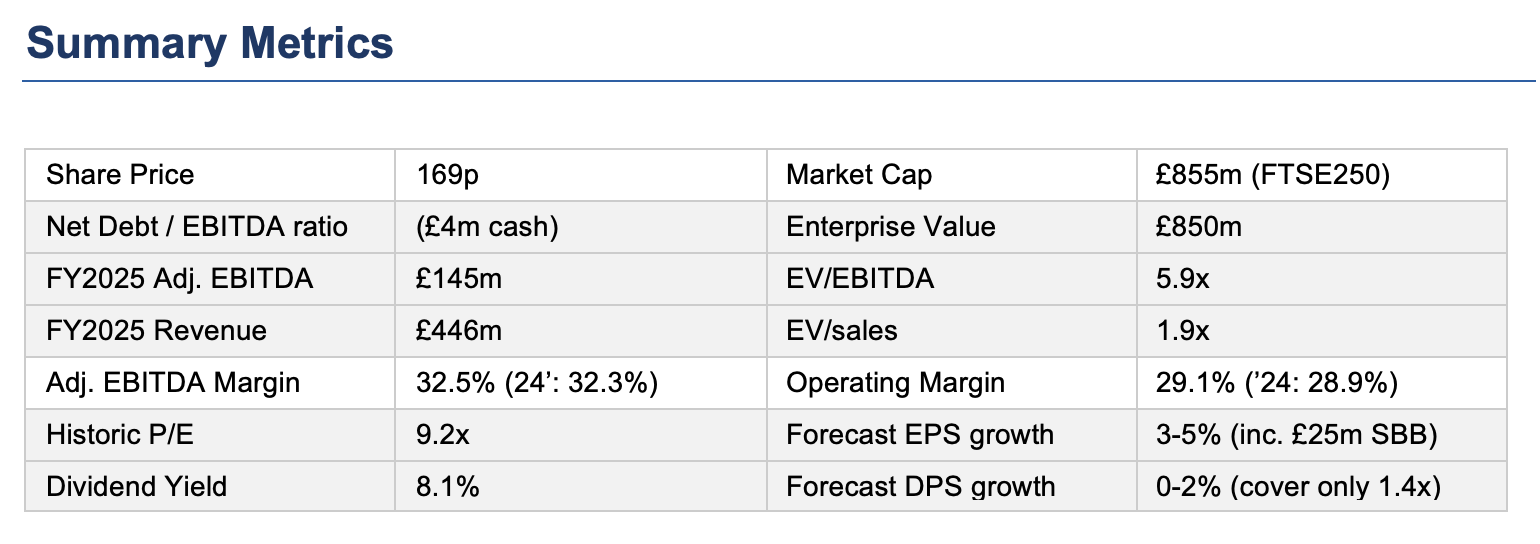

MONY is a decent sized midcap at £850m, albeit they have struggled to generate much investor excitement in recent years.

Technicals & Momentum

A poor chart courtesy of the recent AI-led selloff. Whilst there has been a dead cat bounce this week the shares remain well below their 50 and 200 day MA.

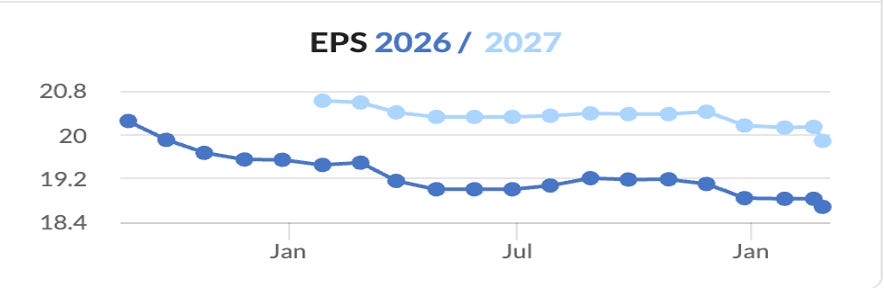

The EPS forecast trend has been one of gradual drift over the past year or so, offset to a degree by the ongoing SBB. Analyst coverage is reasonable with 9 brokers active – price targets range from 173p to 275p – suggesting good potential upside from current levels (see valuation section below)

Guidance & Targets

• 2026 Adj. EBITDA consensus: £146m (range £142m-£153m), implying circa +1% growth from FY2025.

Management guidance (23/2): ‘In line with consensus’. Pretty insipid stuff really

No medium-term financial targets have been formally communicated in terms of margin, revenue growth etc. Another red flag given standards set by other PLCs.

Bull & Bear Drivers

Key Risks

• AI Disintermediation : The most prominent debate in analyst community. Agentic AI (ChatGPT, Google AI Overviews, etc.) could disintermediate PCWs by executing product searches and switches autonomously, bypassing comparison website interfaces. PPC costs rose 21% per unit in 2025 partly because Google’s AI Overview content (non-monetised) is crowding out organic search, funnelling more competition into paid search. Morgan Stanley’s December 2025 downgrade explicitly cited ‘agentic AI overhang’ as a medium-term overhang.

• Insurance Market Deflation: Insurance vertical (52% of revenue) is highly correlated with premium inflation cycles. Following the 2022-2023 car insurance premium spike, the market is now deflationary — premium deflation reduces consumer switching motivation and lowers CPAs. FY2025 Insurance revenue fell 1%.

• PPC Cost Inflation: Google search remains the dominant customer acquisition channel. Structural changes in Google’s search results page (AI content, layout changes) are funnelling competition into paid search slots, increasing cost-per-click. This is a direct gross margin headwind.

• Quidco Margin Drag: The cashback segment’s 13% EBITDA margin compares poorly with the 60-68% margins of core comparison verticals. If Quidco does not achieve its strategic goal of becoming a high-frequency engagement channel that feeds insurance comparison, it will continue to dilute group returns. Management has not communicated a clear Quidco return-on-investment framework.

• Unforeseen regulatory change that restricts comparison pricing, mandates direct-to-provider switching, or creates a publicly funded comparison utility.

Upside Catalysts

• SuperSaveClub continues to scale (target 3-4m members) and member CLTV advantage is sustained, leading to a meaningful uptick in margins and revenues coming from an increased share of wallet from customers using the loyalty scheme.

• PPC cost inflation moderates as Google’s AI Overviews stabilise and MONY’s direct traffic grows.

• Energy switching tailwind persists for 2-3 years as consumers re-engage with the market.

• Mortgage cycle restocking generates meaningful Money vertical uplift as 2020-2022 fixed rate deals mature (2025-2027 peak reset window).

• Consolidation in the PCW market would be a major positive for the MONY investment case. This could be a long time coming but who is to say that GoCompare might not be sold from Future ? However, there is no obvious reason right now for any existing players to buy one of the others.

Valuation Framework

Current Valuation

What is the Market Pricing In ?

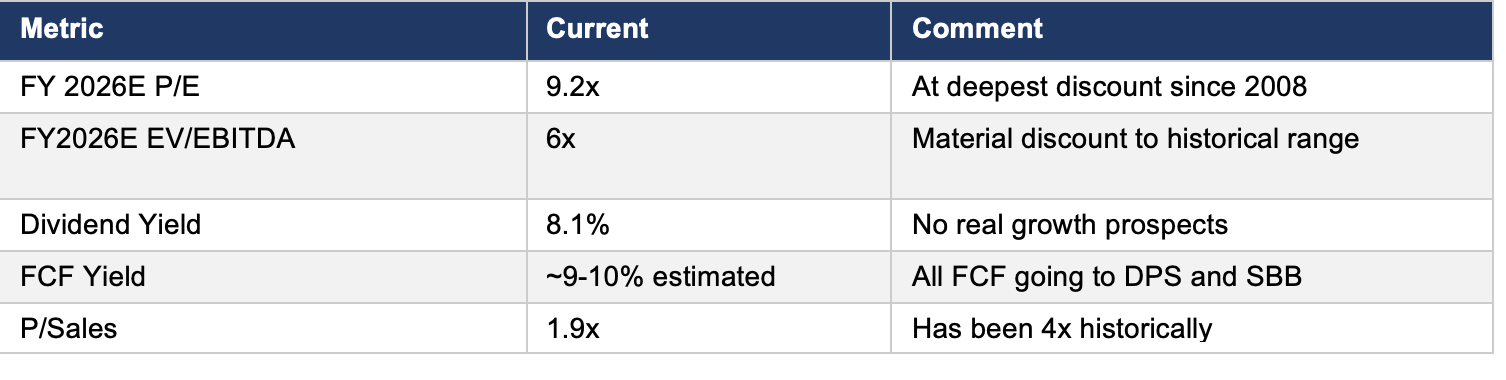

At 169p (£850m market cap), with £145m in EBITDA and near-100% FCF conversion, the market is implicitly pricing some of the following risks :

(a) structural, permanent EBITDA erosion from AI disintermediation

(b) a sustained compression in margins from PPC cost inflation

(c) terminal value degradation of the core PCW model as consumer behaviour shifts.

The 9x trailing P/E is the lowest since the 2008 financial crisis, in the context of a business that just reported its highest-ever revenue and EBITDA.

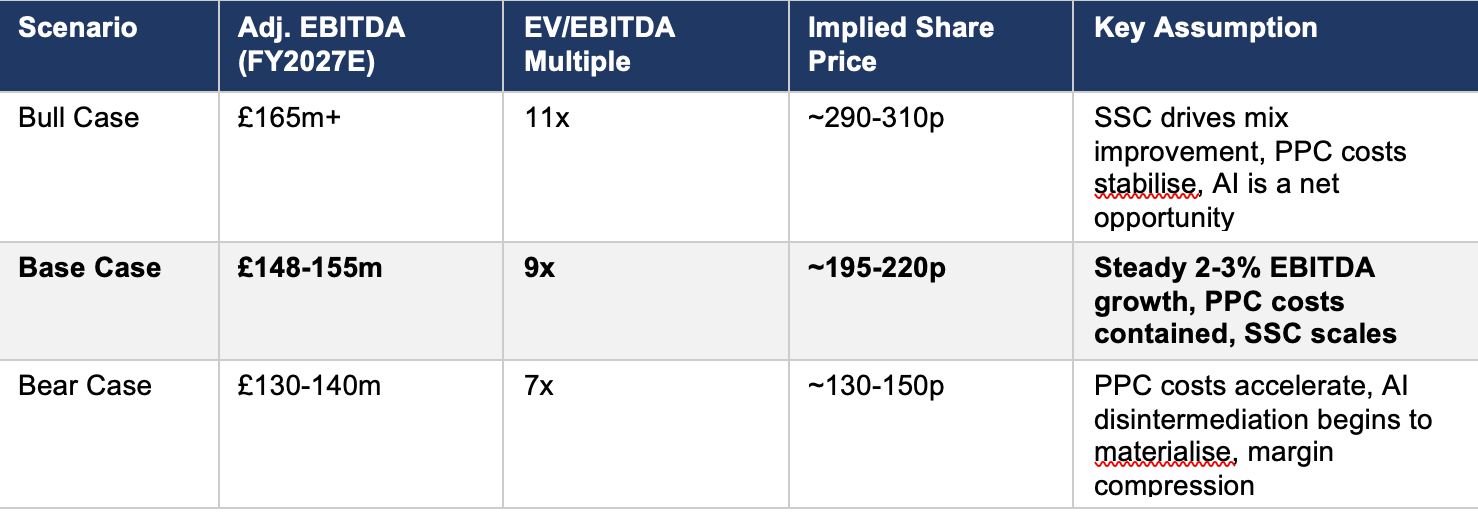

Some Valuation Scenarios

Conclusion

MONY is a high-return, asset-light, cash positive business currently trading around it’s lowest valuation since 2008 despite producing record results this week (albeit with very low growth). It feels that investors are applying an excessive discount to what is an uncertain/unforecastable AI risk which management are trying to manage proactively (eg.ChatGPT partnership). The SuperSaveClub represents a positive response to the ongoing challenges of Google PPC exposure, while energy switching, mortgage cycle tailwinds, and B2B platform growth provide three other growth initiatives which could sustain or grow profitability.

At 169p today’s share price is just above the bear case shown above after a post-results bounce this week. The base case implies 15-30% upside from current levels. The key variables IMO are not near-term earnings — these appear stable — but the trajectory of PPC costs, the credibility of the SuperSaveClub as a margin offset to this and the unknown medium term impact of rival AI solutions.

In summary, MONY is oversold and cheap but with limited growth forecast and weak share price momentum. Margin for error today is high with the SBB, 8% dividend yield and net cash position providing some downside protection. Given the mature earnings profile and already high returns I think it’s best seen as an income stock rather than a compound growth story.

Hi Paul, thanks so much for your comments. The Citrini piece is thought-provoking on a number of levels but we shouldn't lose sight of the fact that, as we speak, it is a very slick narrative rather than evidence. Thoughtpieces like this are arriving on our desks almost daily now and we should always examine their motivations and timescales - the June 2028 apocalypse outlined is conveniently far enough away and Citrini by their own admission does engage in thematic short selling.

Looking at MONY specifically you are right to highlight the friction costs central not only to PCWs but numerous other intermediary type businesses (eg. financial advice, property agents, travel sites, etc). It's also fair to say that PCWs have no inherent moat and switching costs for consumers are almost zero - as I said in my MONY piece 4 PCWs in the UK are at least one too many but I don't know how that gets resolved. You also mentioned Insurify on one of your recent YouTube chats - Insurify is not new and has been around for 10 years in the US now. As far as I can see it has no plans to enter the UK which already has 4 mature PCWs.

I think all aspects of regulation are also very overlooked in the current debates about AI agents eating incumbents' lunches. Do ChatGPT et al really want to become FCA regulated bodies ? Unlikely I would say. Decades of customer data are also not without value here and need protecting.

Whilst the pace of AI capability is escalating rapidly my view is that consumer/corporate inertia means uptake will be slower than the current doomsday scenarios suggest. Will ChatGPT cause hotels, airlines, insurers et al to slash their prices ? Again unlikely IMO. The customer has to have a clear reason to bin things that work well for them already. It's undeniable that PCWs save people money.

The Citrini piece only briefly considers goverment/consumer responses to their taxation base and jobs being hollowed. These responses have yet to be determined but will have to be significant. AI businesses currently have a window of opportunity to justify their current blue sky valuations - doom-mongering very much suits their book but the tide could turn against them just as quickly. Note the ChatGPT funding round last week - basically vendor finance from Amazon, Nvidia etc. All very circular and Ponzi-esque.

As investors we ultimately have to take views in a highly uncertain world. Prices fluctuate considerably more than values but I think with MONY there is a pretty decent margin for error - the markets have already decided it is a loser and whilst the recent link with Chat GPT may be defensive the scope to slash their Google PPC costs to protect earnings is real. At least they are doing something and are alert to challenges.

Thanks for questioning my thesis - this is far more valuable feedback than blind agreement ! As Keynes once said “When the facts change, I change my mind. What do you do, sir?”

I reserve the right to be wrong and change my mind here !

Lots more to debate in all of this. Cheers, Scott

Many thanks Scott.

How do you see MONY faring when - as Citrini Research suggested last week - consumer 'friction costs' (re reason why PCWs exist) when buying insurance, energy, financial services, travel, etc goes to zero?

https://www.citriniresearch.com/p/2028gic?hide_intro_popup=true

"By early 2027, LLM usage had become default. AI agents began to change how nearly all consumer transactions worked. Humans don’t really have the time to price-match across five competing platforms before buying a box of protein bars. Machines do.

Travel booking platforms were an early casualty, because they were the simplest. By Q4 2026, AI agents could assemble a complete itinerary (flights, hotels, ground transport, loyalty optimization, budget constraints, refunds) faster and cheaper than any platform.

Likewise insurance renewals, where the entire renewal model depended on policyholder inertia, were reformed. Agents that re-shop your coverage dismantled [the PCWs] and the 15-20% of premiums that insurers earned from passive renewals."