REIT Petite

The Shrinking UK Listed Real Estate Sector

The contraction of the UK listed REIT sector over the past five years has been dramatic. At its peak in 2019, there were 83 listed REITs on the London Stock Exchange. By early 2026, this number had fallen to approximately 40 — a decline of over 50% in less than seven years. The market capitalization of the sector peaked at over £80bn in 2021 and sits at just over £50bn today. Less than Nvidia’s recently announced $80bn share buyback !

In this article I take a look at what has driven this decline, what’s left today and examine where investors may wish to crawl through the wreckage in search of income and capital growth.

REIT Takeovers 2021-2026

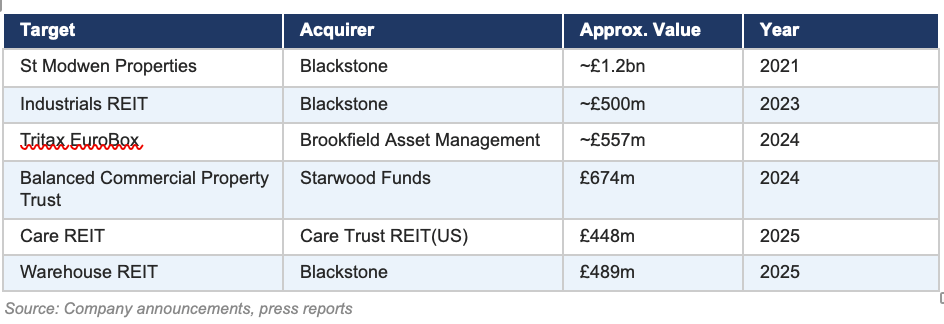

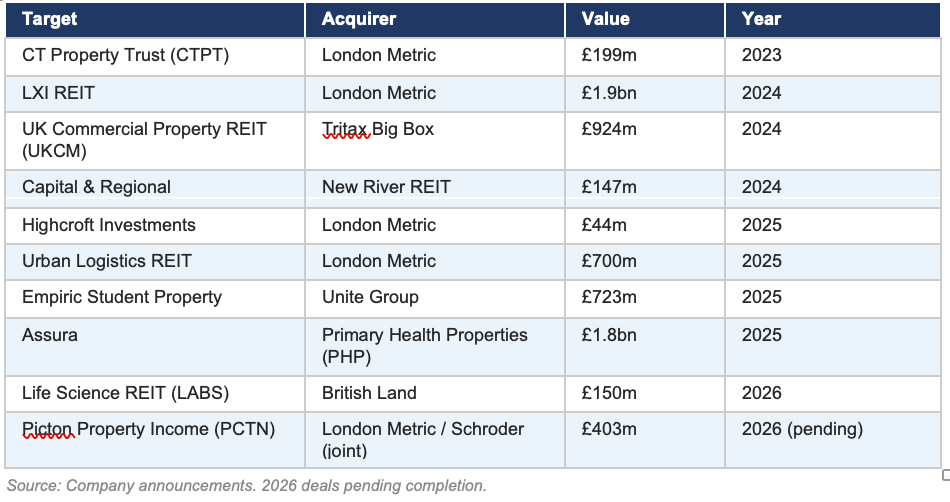

From mid-2022 to the start of 2026, 17 REITs were lost to mergers or take-private deals, and a further 14 wound up or entered wind-down. So far in 2026 British Land has completed a £150m offer for Life Science REIT whilst Picton Property recently received an offer from LondonMetric and Schroder REIT, all of which suggests that the sector could shrink yet further.

As the sector has consolidated there have been two main acquirer groups – private equity and other listed REITs.

Private equity have typically offered all-cash deals that have outbid listed peers. Blackstone alone has taken out Warehouse REIT, Industrials REIT and St Modwen, and also built a significant stake in Tritax Big Box

Within the REIT-on-REIT transactions LondonMetric has been the dominant listed acquirer, transforming itself from a mid-tier FTSE 250 business into an FTSE 100 constituent through a series of well-executed deals. Their current £403m all-share bid for Picton Property Income in conjunction with Schroder Real Estate is the latest in a long line of consolidatory moves. Last year’s battle for Assura between PHP and KKR was also notable, with shareholders opting to stay with a listed vehicle offering inflation linked dividend growth going forward. A rare victory for the quoted sector.

The logic behind these deals is compelling: greater scale leads to lower running costs, higher earnings, lower cost of debt, dividend progression and greater share liquidity. From a valuation perspective the persistent discount to NAV at which most REITs have traded in recent years has allowed for successful bids at discounts to published asset values, with shareholders in many smaller vehicles faced with ‘take it or leave it’ proposals. As gilt yields have risen sharply from low levels higher debt margins, fixed general administration costs and limited secondary market liquidity have weighed heavily on the smaller players, regardless of asset quality.

Performance : UK REITs v FTSE All Share

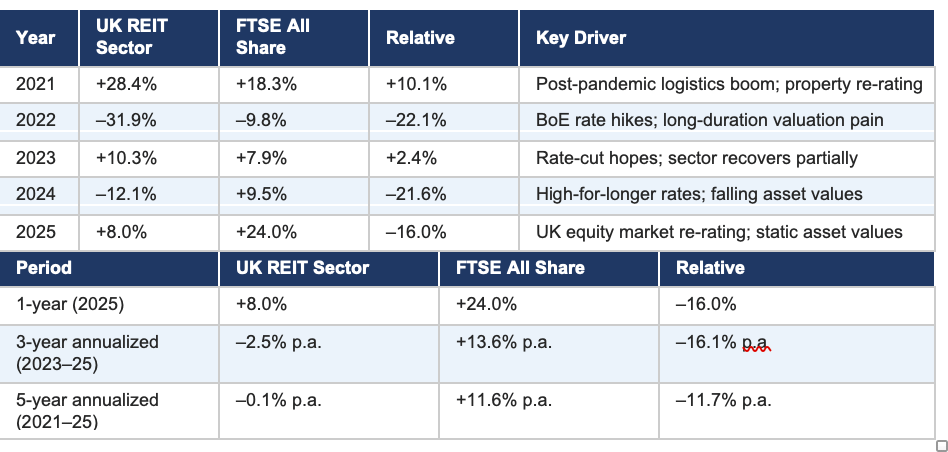

The spate of takeover activity we have seen has not been translated into strong sector performance and acquirers have taken advantage of depressed sector valuations, particularly since gilt yields started to rise in late 2022.

Over the past 5 years The UK REIT sector (via the FTSE EPRA/Nareit UK index) has been a dismal performer relative to the FTSE Allshare with annualised total returns flat against a UK equity market annual return of +11.6%

Why Has the UK REIT Sector Underperformed ?

UK REITs and Gilt Yields – The Key Relationship

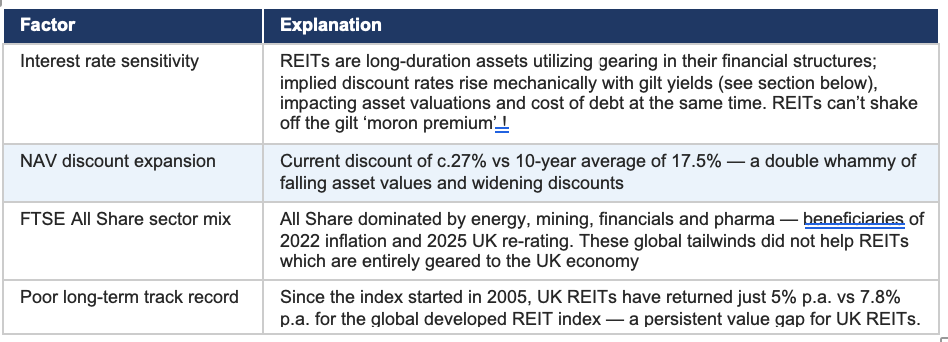

One of the most important factors driving UK REIT equity performance is the level and direction of UK gilt yields, particularly the 5-10-year benchmarks. The inverse relationship is structural: REITs are long-duration assets whose implied present value falls mechanically when the discount rate (proxied by gilt yields) rises.

Three transmission channels explain the sensitivity:

• Valuation mechanics: a REIT’s value is the discounted present value of decades of future rental income. When gilt yields rise, the discount rate applied to that income stream increases, compressing the implied asset value and widening NAV discounts.

• Debt cost pass-through: REITs are structurally leveraged. Rising base rates and gilt yields increase the cost of refinancing fixed-rate bonds at maturity and raise the cost of variable-rate facilities, directly squeezing earnings per share.

• Income competition: at gilt yields above 4.5–5.0%, government bonds become credible income alternatives to REIT dividends of 5–8%. Capital rotates out of REITs into risk-free alternatives, depressing share prices further below NAV.

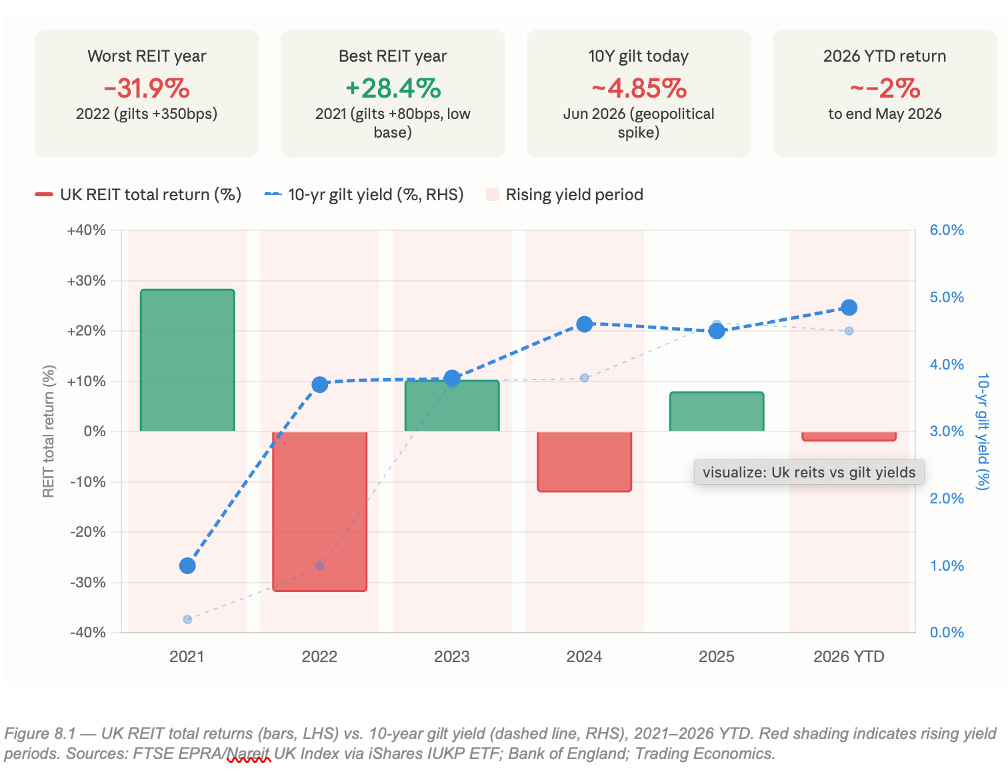

The 2022 experience is the starkest illustration of the gilt-REIT relationship. The Bank of England raised the base rate from 0.1% to 3.5% across 2022 — the most aggressive tightening cycle in 30 years — while global bond markets sold off sharply following the post-Covid inflation surge. The 10-year gilt yield rose approximately 270bps over the year. The direct consequence for UK commercial property values was severe: all-property capital values declined 22% between June 2022 and December 2023 — the sharpest and fastest correction in modern UK real estate history. The REIT sector, as a leveraged, mark-to-market expression of those values, fell 31.9% in total return terms in 2022 alone.

The 2026 picture so far is one of continued underperformance by the REIT sector relative to the broader market, with -2% returns in UK real estate against c.+5% for UK equities to the end of May. The geopolitical shock in March 2026 disproportionately hit long-duration real estate equities at a time of rising gilt yields and UK political turmoil — very similar to the pattern seen in 2022 and 2024. In March 2026, the 10-year gilt yield touched 5% for the first time since April 2008. The real estate sector’s response was immediate and severe. March 2026 ranked alongside March 2020 (Covid) and September 2008 (Lehman) as one of the three worst single months for REIT equities in the modern era. The IUKP ETF fell approximately 8% in March alone, erasing the modest gains made in January and February.

The graphic below covers the relationship with gilt yields over the past 5 years.

The correlation is clear – in both 2022 and 2024 (and more recently in March 2026) REIT returns were sharply negative during periods of rising gilt yields and perceived UK political crises.

UK REITs – Sector Constituents & Valuation

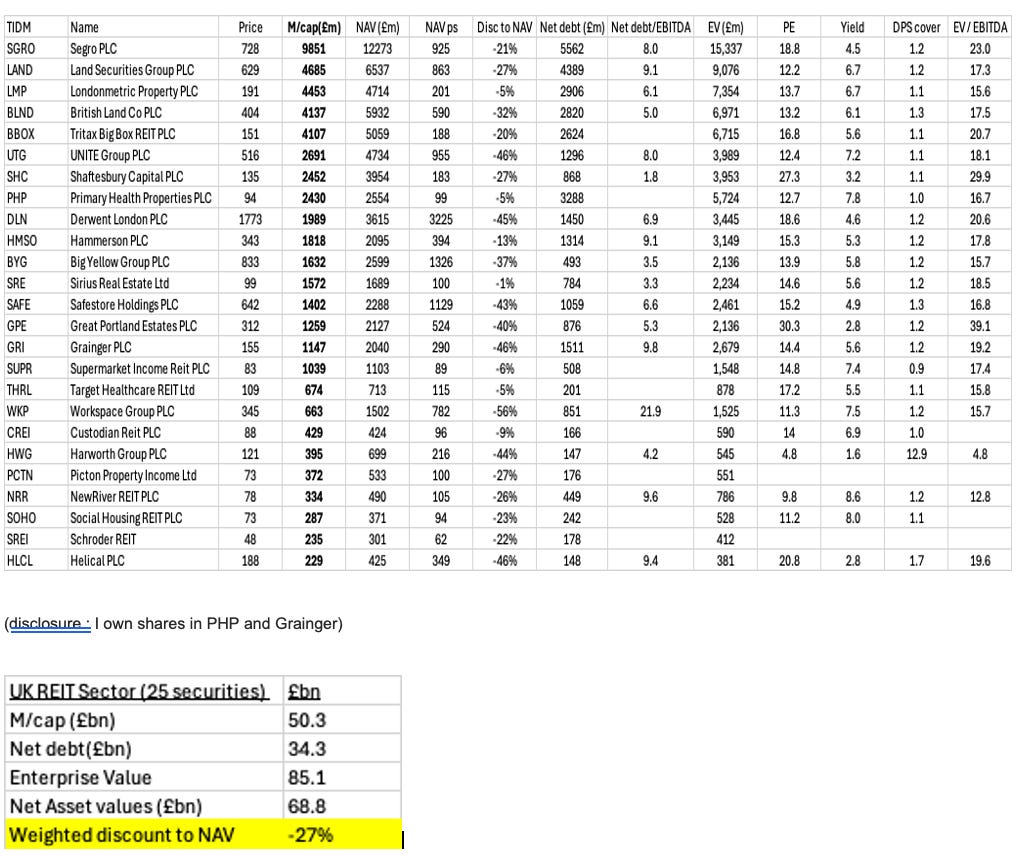

To help drill down into the companies I have compiled an investable universe of 25 stocks with a market cap of more than £200m. Within this list there are 5 stocks in the FTSE100 – Segro, Land Secs, Londonmetric, British Land and Tritax Bigbox – and a further 11 businesses with market caps of >£1bn. The following table gives a summary of some key metrics for the sector (source : Sharescope)

High levels of debt relative to EBITDA are a notable feature for most REITs as are the elevated discounts to NAV, even taking into account a significant drop in most real estate values over the past three years as gilt yields have soared. UK REITs must also payout at least 90% of their qualifying rental income profits as dividends hence the very thin cover ratios across the sector.

Other important factors to consider which are not shown in the table above include :

LTVs – as a rough rule of thumb 20% is seen as very good and >40% as bad for listed REITs. Most have stated targets to be in the range of 30-35%.

Cost of debt – a key challenge as REITs refinance into higher 5 year swap rates over the next few years and lose fixed rate protections. Many quoted REITs are still able to show all in debt costs of 3-4% for now but in most cases this is not sustainable in the long term without help from the gilt market. Unlikely as we sit here today.

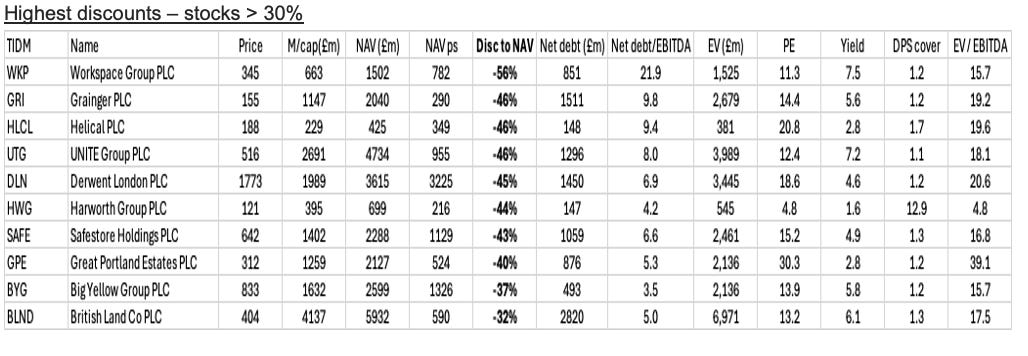

The sector offers a wide array of exposure to real estate by subsector and size but I think it is worth highlighting the stocks offering the most extreme asset discounts. These tend to be found in the offices and self storage sectors although specialist niches such as student (Unite) and BTR (Grainger) also feature. The group below could potentially have significant scope for recovery in more benign times, particularly if gilt yields peak and underlying real estate valuations improve.

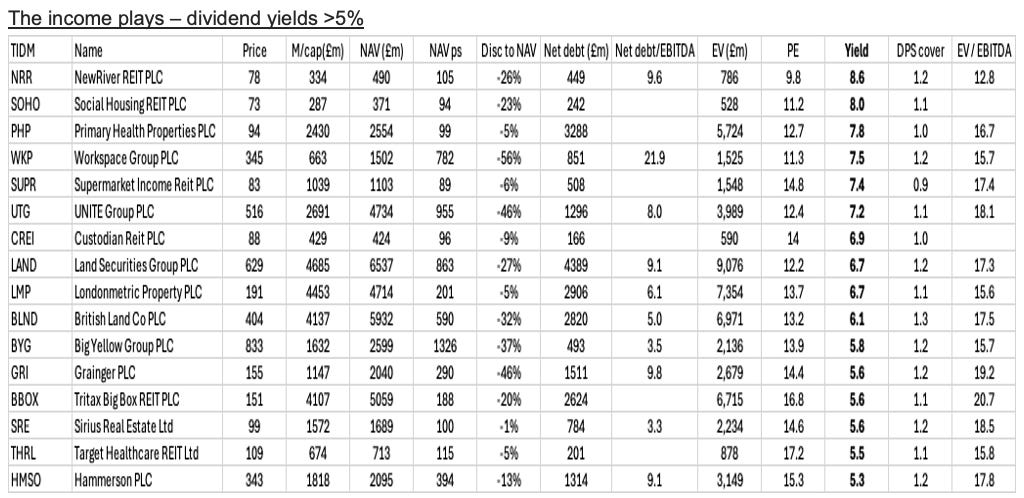

The sector also has strong income attractions with 16 of the 25 currently offering dividend yields in excess of 10 year gilts. Very few on the list are seeing falling rental income despite pressure on valuations, which suggest that most yields are sustainable. Some of the strongest businesses in the sector such as PHP and Londonmetric have excellent track records in delivering dividend growth in real terms too, making them very suitable total return alternatives to gilts.

UK REITs – Key Themes & Outlook

The pace of M&A shows no sign of abating. With the £403m bid for Picton in May 2026, Workspace Group under activist pressure and numerous smaller vehicles still trading at wide discounts, further attrition is likely, particularly in the extreme discount businesses. PE buyers remain active acquirers of UK commercial real estate. The flow of assets from the listed to the private market at discounts to NAV remains a persistent feature of the landscape. While this reduces investor choice in the listed space, it should provide a floor on valuations for quality assets.

A re-rating is possible if the gilt market behaves and base rates remain stable. Against this political risk is likely to remain elevated (‘the moron premium’) as the Labour party continues to implode. Historically, purchasing UK REITs at a 30% discount to NAV has delivered a positive one-year return 95% of the time. The current period of wide discounts may represent one of the better entry points of the cycle. This would be compounded by improving real estate asset values from currently depressed levels, with gearing to LTV kicking in.

The bifurcation between winning and losing real estate asset classes is widening. Industrial and logistics, prime London offices, supermarkets and healthcare remain the structural beneficiaries — and these are the subsectors where most remaining listed REITs have concentrated. Meanwhile, secondary/regional offices and non-prime retail continue to face headwinds. The jury is very much out on smaller niches such as PBSA and BTR as evidenced by the huge discounts applied to Grainger and Unite

The UK REIT sector remains very much one for the contrarian and it’s dependence on a better gilt market and more stable politics feels like the wrong place to be for now. However, the combination of safe dividend income and large asset discounts in a rapidly consolidating sector should ultimately reward the patient buyer today.

If stock selection feels too difficult then the ETF below might just be a nice way to wait for the recovery.

everyone talks about the winners, but surviving the losers matters too