Old MacDonald Has A Plan

A Detailed Look at BRK.L

(Disclosure: I own shares in Brooks Macdonald Group plc)

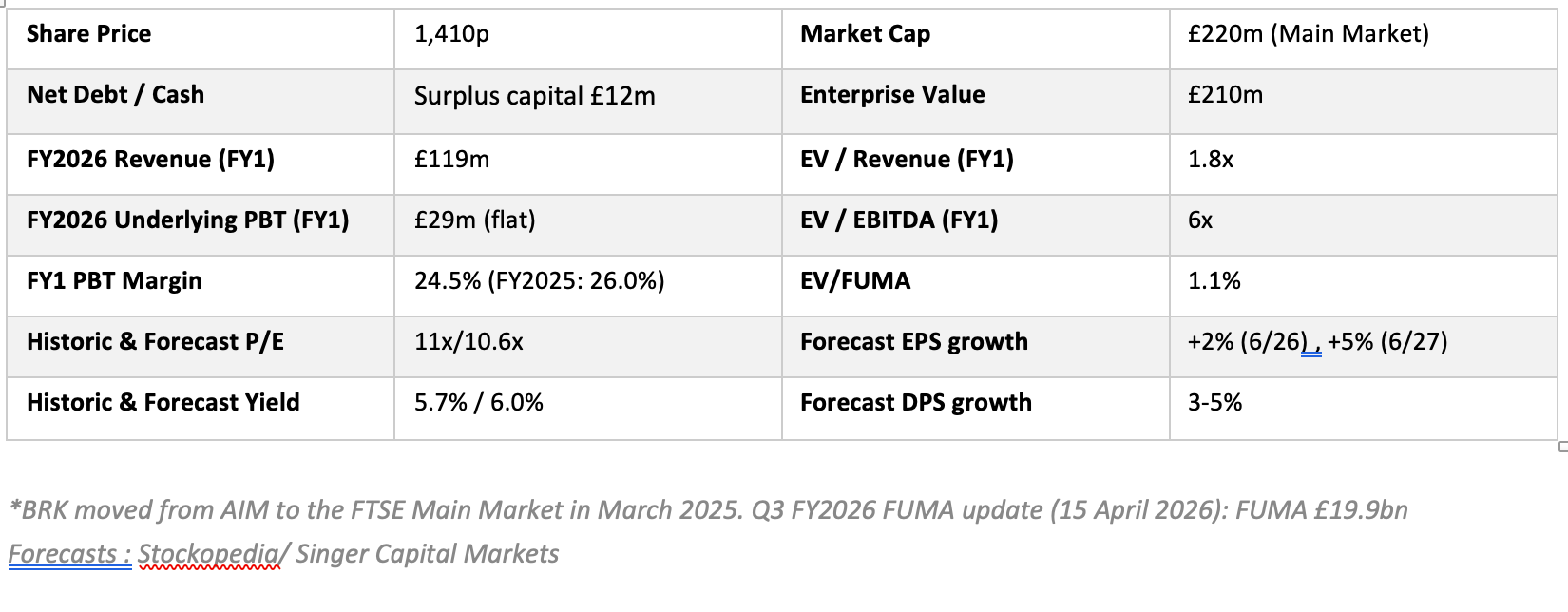

Summary Metrics

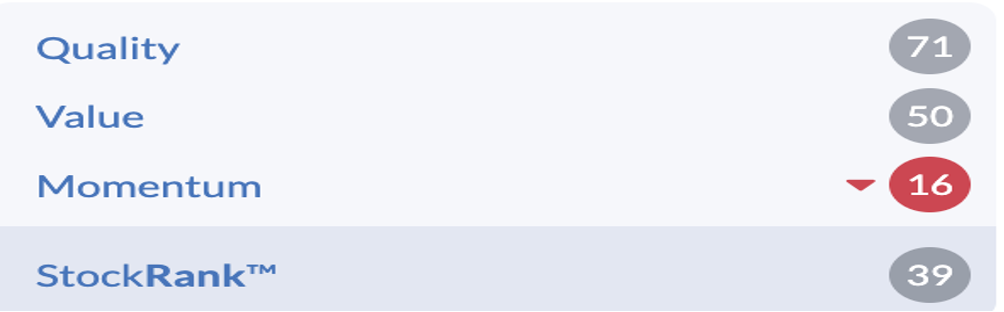

Stockopedia Stock Ranks

Risk rating : Balanced

Stock style : Neutral

Business Overview

Brooks Macdonald is a UK-focused wealth management group providing discretionary investment management, financial planning, and managed portfolio services. BM has £20bn of funds under management and advice (FUMA) with it’s dominant distribution channel being independent financial advisers (IFA’s) who account for 75% of FUM. Under new CEO Andrea Montague the strategy has evolved significantly over the past two years with the sale of the offshore business and a series of acquisitions building up the financial planning segment — now under the Brooks Financial sub-brand — in an attempt to move upstream and own the advisory relationship as well as the investment management mandate. There has also been wholesale management change at a senior level as well as a move from AIM to the Main Market which took place last March. Whilst all of this is admirably forward facing it has yet to be translated into a meaningful improvement in results and the share price has been broadly flat over the past year.

Key Timelines

• 1991 (Founded): Chris Macdonald & three partners launched the firm as a boutique HNW manager. FUMA £250m by 1993; IPO on AIM in 2005 with FUM c.£1bn.

• 2007–2010 (First acquisitive phase): Lawrence House (2009), Braemar Group (2010) and regional office expansion drove FUMA past £2bn and enabled the first dividend.

• 2017–2021 (Management disruption): CEO Caroline Connellan’s restructuring programme led to turnover of senior managers and a period of net outflows.

• 2021–2023 (Recovery and pivot): Recovery under Andrew Shepherd; a series of acquisitions began the financial planning pivot. Net flows returned to positive.

• 2022–2024 (Net outflow cycle): Rate cycle headwinds , competitor MPS pricing pressure and management disruption produced sustained net outflows through FY2024 and H1 FY2025.

• FY2025 (Strategic reset): Sale of Brooks Macdonald International for up to £51m. Reinvested c.£50m in financial planning acquisitions (Lucas Fettes, LIFT-Financial, CST Wealth Management) under new CEO Andrea Montague. Brooks Financial sub-brand launched. Move from AIM to FTSE Main Market (March 2025).

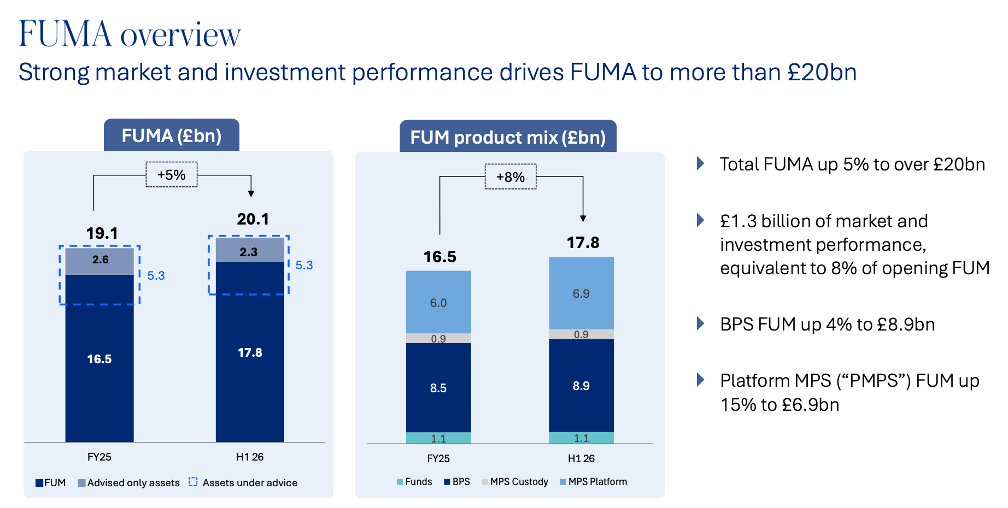

• FY2026 9mths (Flow inflection): FUMA crossed £20bn for first time; net flows turned positive for first time since H2 FY2023. H1 Revenue +12%.

Divisional Structure / Revenue Mix

• Bespoke Portfolio Service (BPS 50% of FUM): bespoke discretionary business serving private clients via the IFA channel. Higher-touch, higher-yield service (70 bps) but structurally challenged – FY26 will be the fourth consecutive year of outflows here, averaging -£450m p.a.

• Managed Portfolio Service (MPS, 39% of FUM): Standardised model portfolios on the IFA platform. Platform MPS assets grew 15% in H1 FY2026; revenue +22%. Lower yield (22bps) but scalable — incremental AUM requires minimal additional headcount benefitting operating margin. MPS is the primary net flow engine, having averaged £750m of net inflows over the past four years.

• Brooks Financial (financial planning, £5.3bn advised assets): Built by M&A in recent years. Of the £5.3bn advised, 56% is also managed by Brooks (up from 51% a year prior).

• BM Funds (6% of FUM). Own managed multi-asset funds, but seeing steady AUM erosion in recent years.

Revenue Growth Drivers

BRK’s revenue growth depends heavily on net flows and market movements. With 25% of revenues now in advice intra-group cross-sell and new product developments such as Retirement Strategies are set to become increasingly important too.

FY2025 delivered a strategic reset: disposal of International, three financial planning acquisitions, and a return to positive FUMA growth. Recent results have therefore been heavily distorted by M&A/ disposals. In H1 FY2026 net flows turned mildly positive and revenues grew by 12% but there was no disclosure of the underlying revenue growth. My guess is that it was barely positive

Revenue estimates for FY2026E point to full-year revenue of ~£115–120m, implying H2 broadly in line with H1.

Management has set a medium-term net flow target of >5% starting FUM annualised — this equates to almost £1bn a year. Singers forecast revenue growth of 5% and 7% for FY27 & FY28 but this assumes they get to the c.£1bn flow target in both years – a very big ask from the barely-positive current level.

Margins & Returns

Profit Margins

• Underlying PBT margin (H1 FY2026): 23.4% — down from 29.7% in H1 FY2025 . The compression reflects three deliberate cost layers: (1) investment in technology and AI automation; (2) financial planning acquisition integration costs; (3) head office relocation costs (£1.2m dual running in H1). Management’s H2 cost guidance (broadly flat on H1 ex-FSCS levy) and full-year guidance in line with consensus implies some H2 improvement. Singers forecast 24.6% margin for FY26

• Revenue margin: Revenue yield fell from 59bps to 51bps in H1 – BPS 70bps, MPS 22bps. Reflects lower transactional & interest income as well as the ongoing structural shift towards MPS. Management expects yield to stabilise in the 48–52bps range.

• Cost discipline: Underlying costs grew only +3% in H1 FY2026 despite heavy strategic investment – this comes after realising a £3m annualised saving from the previous restructuring programme.

Bottom line: at 23.4%, BRK’s PBT margin is at a multi-year low. Whilst much of this reflects recent investment for growth it has to represent a low point for investors given their peer group (eg. Rathbones current 26%, target 30%). A margin pathway to 27%+ by FY2028 is possible if net flows reach 3–5% annualised and the cost base grows at <5% but there is no formal target out there.

Returns

ROCE for FY2025 was 21%, having fallen from 25% the previous year. ROCE looks set to fall again in FY26, reflecting the current investment phase drag. I wonder also if recent acquisitions have been dilutive for returns – the acquisition of LIFT for £30m (plus £15m earnouts) was seen as pricey at the time. Historically BRK has generated ROCE of 25–30%+ in normalised conditions, underpinned by the asset-light, fee-based model. No formal ROCE target has been published so falling ROCE is definitely something to keep an eye on; like margin it needs to improve from here.

Industry Structure & Competition

The UK wealth management market is a structurally growing but intensely competitive market. The UK retail wealth management market manages approximately £600–700bn in discretionary and managed portfolio assets, within a total professionally managed wealth pool of £1.5–2 trillion. Platforum estimates the TAM for advised clients is £1.1 trillion

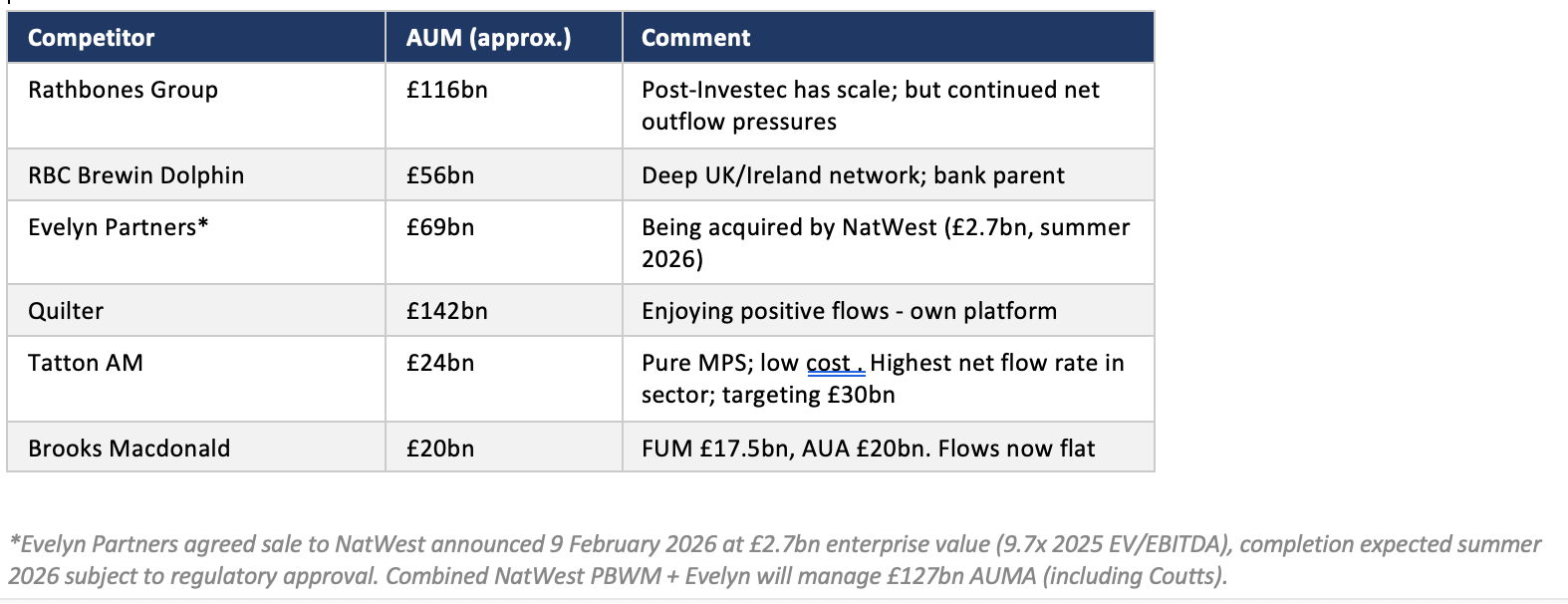

The WM market has been consolidating for many years : Brewin Dolphin was acquired by RBC (2022), Rathbones merged with Investec Wealth (2023) and more recently Natwest acquired Evelyn Partners for £2.7bn, whilst IFA roll-up activity continues at pace. This consolidation backdrop leaves mid-tier operators like BRK potentially vulnerable to takeover but so far Brooks have been the bridesmaid not the bride.

BM suffers, like many in this sector, from a ‘me-too’ offering and the key question is whether it can use it’s more modest scale to grow more quickly than the large groups now that it has reenergized the senior management team and reset the group strategy.

Cashflow, Balance Sheet & Capital Allocation

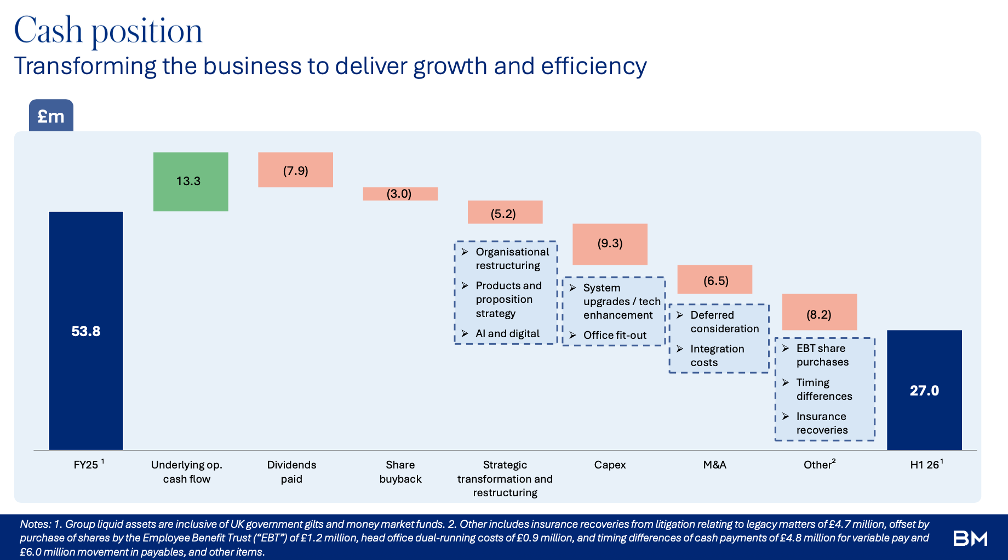

Balance sheet: Net cash of £27m at H1 FY2026 (down from £54m at H1 FY2025), capital surplus £12m (down from £16m at FY2025 year-end).

Cash flow: The wealth management model is inherently cash generative — minimal working capital, low capex, no inventory. FY2025 free cash flow was approximately £28–32m before M&A and dividends but the FCF at the interim stage was undeniably poor, with significant exceptional items, abnormally high capex and the dreaded ‘other’ category all muddying the waters. Capex should fall materially in FY27 from £10m to a more normal £3m, alleviating some of the pressure. In normalised conditions, FCF should represent 80–90% of underlying PBT. It’s imperative that BRK have a ‘clean’ year in FY27.

Dividends: An important part of the investment case for BRK. Grew at 3% at the interim stage extending the 21-year consecutive dividend growth record which is testament to the durability of earnings here. Cover on adjusted eps is 1.6x but cash cover this year is just over 1x due to high capex and restructuring costs.

M&A strategy: BRK has historically pursued bolt-on acquisitions of IFA firms using earn-out structures . The Brooks Financial buy and build (three acquisitions in FY2025) took this to a higher level with advice now 25% of revenues. Management has explicitly signalled appetite for further financial planning acquisitions, subject to quality and cultural fit. As a medium sized WM it is also possible that Brooks may look to merge or be acquired as such groups look to scale further.

Management, Governance & Shareholders

Andrea Montague, CEO (October 2024): Joined as CFO in August ‘23. Previously Group CRO at Aviva, Deputy Group CFO at Royal London. A very busy first 18 months as CEO has delivered the international disposal, three acquisitions, the Main Market move, the restructuring programme, and a return to positive flows. Quick pace of change !

Katherine Jones, CFO (November 2024): Joined from Phoenix Group as Group Finance Director.

Maarten Slendebroek, Chairman (appointed 2023): Former CEO of Jupiter Fund Management, operational experience is highly relevant for a business which has seen significant organizational change and challenging fund flows.

Incentives & Governance

• Incentive alignment: Management KPIs are linked to net flows, revenue growth, and underlying profit — fair enough. The 21-year consecutive dividend growth record creates implicit commitment to progressive capital returns

• Governance improvement: Board was substantively refreshed 2023–2024. Main Market listing (March 2025) now requires full UK Corporate Governance Code compliance — an upgrade vs. the AIM regime

Key Shareholders

The CEO & CFO own very few shares, way below the 200% of salary target – a real red flag for me (see table below).

The Chairman recently bought c.£100k at 1450p and an NED bought almost £400k at 1515p in March 2026. A bit more like it.

Post the move from AIM in 2025 there has been a significant change in the register which has become highly concentrated with Gresham House, Liontrust and Aberforth holding almost 50% of the equity between them. The latter bought during the move to Main List whilst Liontrust’s issues with fund outflows are well documented – they have been selling. The 24.5% held by GH is notable in what is an illiquid share – what is their exit strategy here other than a takeover ? At £220m market cap BM is a long way from the FTSE250 today.

Technicals & Momentum

The shares have gone nowhere over the past year despite navigating the move from AIM well ahead of others. This reflects broader liquidity issues in UK small-cap markets as well as scepticism about the prospects of flow recovery. The shares trade below the 50-day moving average and other than some recent director buying the technical support is currently weak.

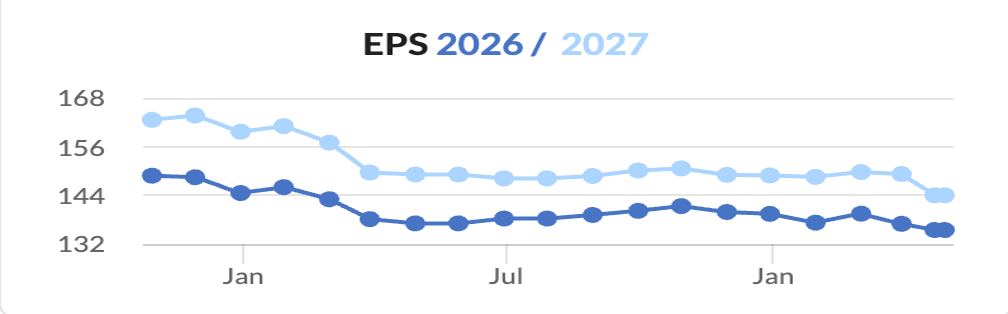

Earnings Momentum

The EPS forecast trend has drifted steadily over the past year as inflows have failed to materialise and investments in growth have escalated. Analyst price targets range from £18 to £25 but overall there has been a lack of new impetus for the story here.

Guidance & Targets

• Medium-term net flow target: >5% annualised net flow rate. (equates to c£1bn of net inflow per annum)

• BAU cost growth: <5% per annum. H1 FY2026 underlying costs +3% — on track.

• FY2026 full-year guidance: In line with market expectations (reiterated at H1 results and implied by Q3 FUMA update). H2 costs ex-FSCS levy guided broadly flat on H1. H2 investment spend roughly half H1 levels.

• Margins: Management has guided that the investment phase cost profile will moderate in H2 FY2026 and into FY2027, with the expectation that margin recovery toward 27%+ will become visible by FY2028. However no formal targets set so far.

Bull & Bear Drivers (1–2 Year View)

Key Risks

• Positive net flows don’t materialise : The investment case rests heavily on this metric. BM are currently way below the >5% target and earnings growth will be moribund without it

• Revenue yield compression: Yield fell from 59bps to 51bps in a single half-year. The risk is that BPS falls quicker than MPS grows

• Weak cashflow : Cash in H1 deteriorated significantly due to lots of one-off items.

• Gearing to weak equity markets : a sector rather than stock specific risk which can lead to earnings downgrades

Upside Catalysts

• Positive net flows do materialise : getting close to the 5% of FUM flow target would be the most powerful re-rating catalyst — shifting the stock from ‘ex-growth’ to ‘growth’

• PBT margin recovers: would de-risk the investment case and demonstrate resilience v peers

• M&A optionality: At 1.1% of FUMA, BRK is modestly priced for a larger domestic or international wealth manager seeking UK scale. Shouldn’t form a central part of the investment case but provides a significant valuation floor.

Valuation Framework

Current Valuation

What Is the Market Pricing In?

I believe that the market is pricing BRK as a structurally challenged mid-tier wealth manager with poor prospects of improving net flows — this can be justified given their recent history but gives no credit for any eventual turnaround. Essentially investors are demanding evidence of this before re-rating the shares.

The 6% forward yield implies either that the dividend is at risk or that this is purely an income stock with no growth prospect.

My best estimate is that the market is pricing a scenario in which net flows remain in the 0–1% range and margins stay around 22–24% — broadly flat earnings — rather than the >5% flow rate and 27%+ margins that constitute management’s ambition. This represents a very low bar to hurdle given today’s share price

Conclusion

The BRK investment case is centred on whether the ‘Reignite Growth’ strategy — with net flow recovery as its primary metric — will create value and take BM from a structurally challenged mid-tier operator into growth mode again.

Investors remain sceptical and value the shares near multi-year lows at 1.1% of FUMA and 11x FY2026E earnings. At 2.0–2.5% of FUMA (a reasonable yardstick for growing peers) BRK could be worth £23–30 per share (ie. double todays valuation) if they execute strongly.

To justify such a meaningful re-rating there are two things that must be demonstrably achieved:

• Sustained net flow recovery: consistently positive flows across multiple quarters, building toward 5% annualised — demonstrating that the IFA distribution rebuild and financial planning cross-sell are structural growth drivers.

• Margin recovery: PBT margin is currently depressed at <24%. Getting toward 27%+ by FY2028 would demonstrate BRK is up there with peers again.

Brooks Macdonald shares have gone nowhere for 10 years and the evidence of a return to growth remains fragile. It’s not a structurally broken business but one hopefully in early-stage recovery. After a significant strategic overhaul over the past two years FY27 will be the first clean year where management can demonstrate that their plan is leading to improved cashflow, profits and a return to growth. If this can be achieved the upside is substantial and the risk/reward profile today looks compelling, supported by a 6% dividend yield whilst you wait.