Bureau De Change

A Closer Look at MAB1.L

I appeared as a panellist on Mello Monday last week , discussing my recent purchase of Mortgage Advice Bureau. The following article is a deeper dive into the idea. The recorded discussion is available to registered Mello users below :

(Disclosure : I own shares in Mortgage Advice Bureau plc)

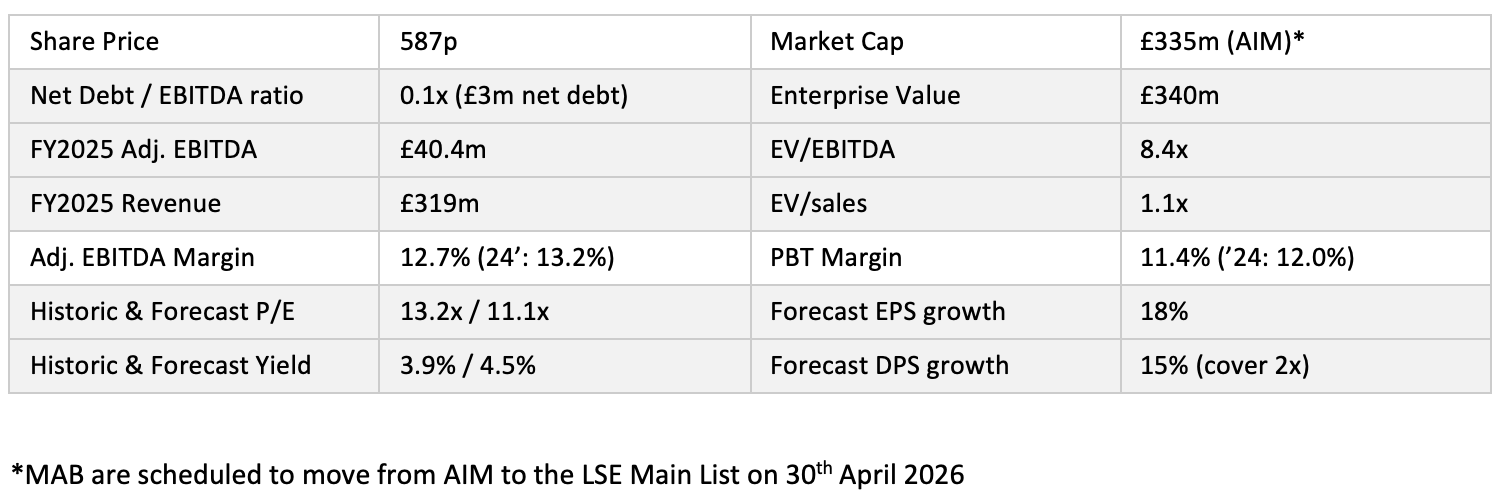

Share price as at COB 16/4/26

Summary Metrics

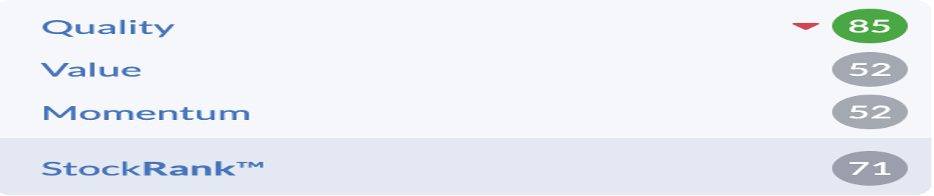

Stockopedia Stock Ranks

Risk rating : Speculative

Stock style : Neutral

Business Overview

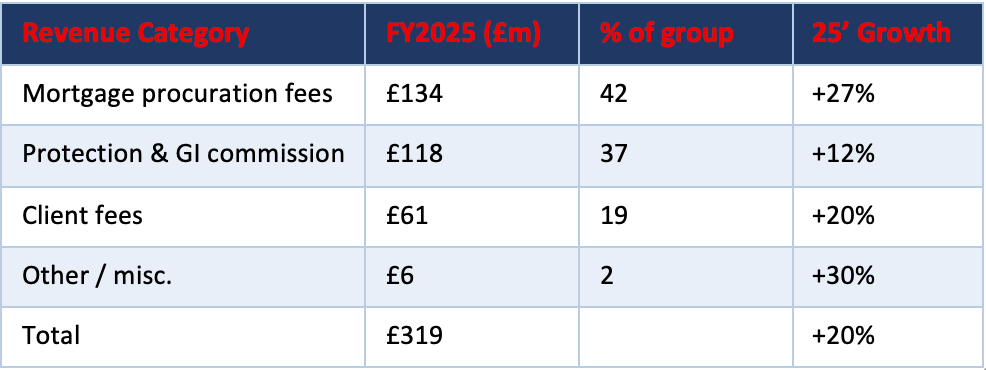

Mortgage Advice Bureau is one of the largest mortgage intermediary networks in the UK with 2,135 advisors and is a leading intermediary brand in a highly fragmented market. The group operates a multi-channel approach comprising a network of appointed representative (AR) firms and wholly owned invested businesses (IBs) offering advice on purchase, remortgage, product transfer, and insurance protection products. Total mortgage completions in FY2025 for MAB were £32bn, representing 5.8% of all UK gross mortgage lending (market share is 8.4% excluding product transfers). Revenue is driven by procuration fees (lender-paid commission per completed mortgage), client fees (mainly in specialist lending), and protection/general insurance commission.

Key Historic Events

• MAB founded in 2000 by Peter Brodnicki. Brodnicki, previously Business Recruitment Director at L&G, acquired a stake and reoriented the business toward a hybrid broker-network model from day one. He remains the CEO and largest shareholder in MAB to this day.

• 2009–2012 (Diversification): MAB expanded beyond estate agencies into new sectors through strategic investments and JVs, including the acquisition of Mortgage Talk in 2012. The multi-channel expansion strategy that defines MAB’s growth model was established in this period.

• 2014 (IPO): Listed on AIM in November 2014 at a price of 160p. MAB then established a record as a compound growth stock at a time when advisor penetration of the mortgage market increased significantly post the FCA Mortgage Market Review in 2014.

• 2022 (Fluent Money acquisition): MAB acquired 75% of Fluent Money Group for ~£73m — a step-change in the invested business (IB) strategy, adding specialist lending, a lead generation platform and later-life mortgage capabilities. This was a complicated transaction with numerous earnout clauses - by their own admission the timing could have been better with the business falling into loss during 2023. Despite this poor start management have successfully turned Fluent around , with margins well above group average. MAB now own 84% with options to purchase the remainder.

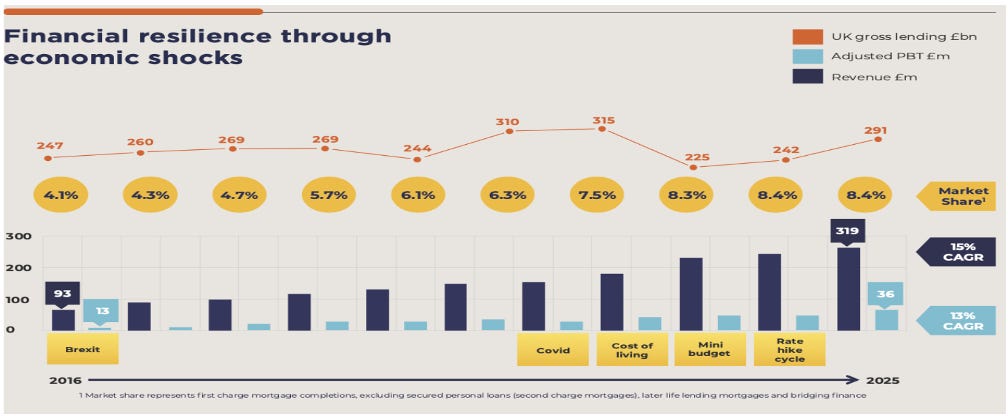

• 2022–2023 (Rate cycle headwinds): The Bank of England’s rapid tightening to 5.25% suppressed mortgage volumes, particularly purchases and remortgages. Revenue growth slowed materially and profits fell in 2023 for MAB. However the adviser base was retained and protection revenues held up, demonstrating structural resilience.

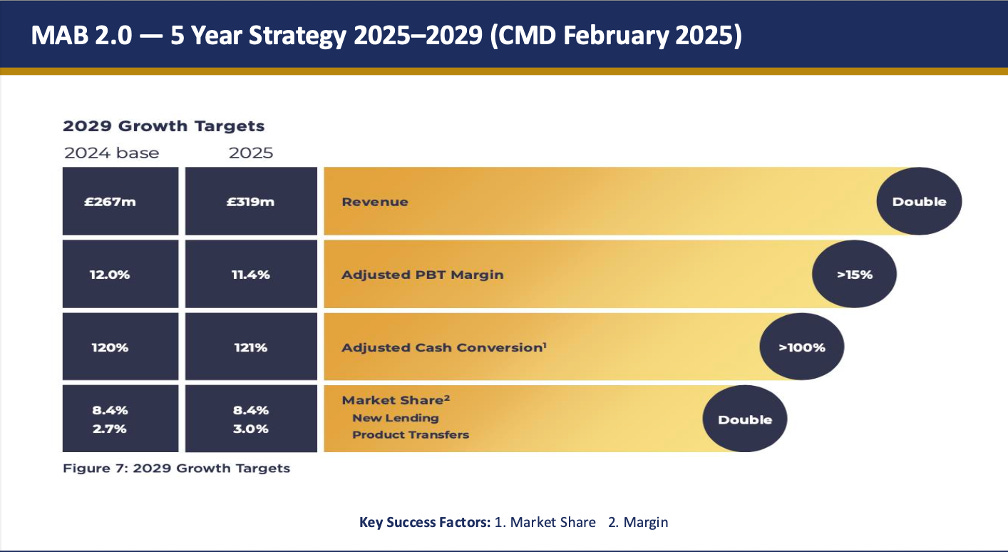

• 2025 (MAB 2.0 launch): At a CMD in February Brodnicki launched MAB 2.0 — a five year strategic framework targeting a doubling of revenue from the 2024 base by 2029, >15% PBT margins, and doubling market share.

Divisional Structure / Revenue Mix

• AR Network (45% of gross profit, 56% of revenues, ~75% of adviser count, 25% gross margin): c.200 appointed representative firms operating under MAB’s regulatory permissions on a revenue-share platform model. Approximately £122k revenue per adviser. Growth in AR firms is capital-light for MAB and comes with very low levels of fixed cost.

• Invested Businesses (IBs) (55% of gross profit, 44% of revenues, 25% of advisor count, 38% gross margin,): MAB-controlled firms where they own a full economic interest. £248k revenue per adviser is significantly greater than the AR route. Higher margins and productivity reflect operational control, cross-sell capability, and head office integration. The focus on the IBs does however requires more capital and fixed costs so it’s a higher risk/reward strategic shift in my view.

Revenue Growth Drivers

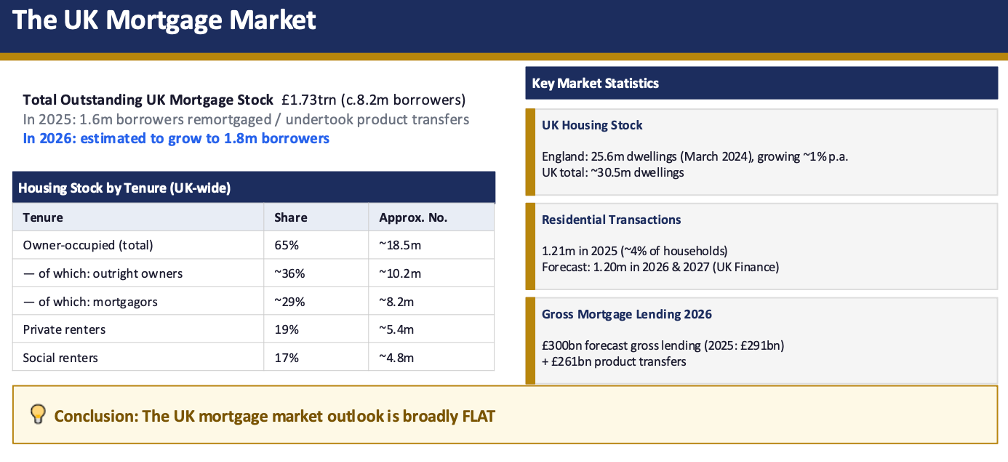

The UK mortgage market is not a growth market (see table below) and advisor penetration is already high at over 80%.

The MAB investment case therefore is heavily dependent on market share growth, with the MAB 2.0 strategy targeting a doubling of share from 2024-2029. Whilst the long term record of MAB in growing revenues and market share is strong (see chart below) their share of the market has stalled in the past two years, leaving them with lots to do over the next four years to hit their targets.

In response their strategy has been evolving with an acknowledgment that product transfers and remortages will be key to expanding their reach, given the current weakness of the new housing market ,where MAB has a share of over 20% already. They are particularly under-represented in product transfers, which is a £260bn market in 2026 but where they only have a 3% share.

During the first year of MAB 2.0 in 2025 revenues grew by 20% driven by: (1) mortgage volume recovery as the rate cycle turned; (2) adviser count expansion (+10% to 2,135 mainstream advisers); (3) productivity improvement (+13% revenue per adviser to £157k); and (4) a full-year contribution of invested businesses acquired from 2022-2024.Protection revenue growth (+12%) remains fairly steady — it grows alongside advice volumes but with annual reviews is less reliant on the broader mortgage market cycles.

Revenue estimates for FY2026E are c.£360-380m, implying 10% growth , which feels achievable given that 65% of their market is concerned with refinancing, where around 1.8m mortgages are set to reprice in 2026 (v 1.6m in 2025). New mortgages are c.35% of MAB’s market but attract about 100% of investor commentary !

Margins & Returns

Profit Margins

• Adj. PBT margin (FY2025): 11.4% — way below the group’s long-run aspiration of >15% by 2029. The fall relative to prior years reflects 1) a poorer mix (refi margins are lower) 2) deliberately elevated IB integration costs and 3) increased head office investment. Management guides a clear pathway: IB admin cost ratio peaks in FY2026, declines from FY2027, and margins trend toward 15%+ by 2029 as revenue scales over a more fixed cost base than they had in the past.

• Gross margin (FY2025): 28.8% (FY2024: 28.8%). Stable, albeit with a marked difference between the two divisions.

• Admin expenses: +23% to £56 m in FY2025. MAB has large central/head office costs covering the technology platform, compliance, marketing, finance, and M&A functions with the growing IB segment driving the largest increase. Excluding IB integration, organic admin growth was modest. The absolute admin ratio (17.6%) is expected to be the high-water mark.

Bottom line: at 11.4%, MAB’s PBT margin looks modest vs. well-run financial services platforms. But the margin compression has been deliberate — the history of MAB has been one of investing and expanding during downturns which is effectively what has happened from 2022 to 2025. The margin pathway to >15% is arithmetically clear, driven primarily by operational gearing , with the Invested Businesses mix rising as a proportion of group revenue , utilising head office investments more efficiently as the platform scales. In addition to this revenue growth and productivity gains from digitalization of the platform could also be material contributors to improved margin.

Returns

ROCE (FY2025) was 34%, up from 32% in FY2024. This is a strong metric for a financial services business at scale — reflecting MAB’s asset-light model and targetted acquisition approach as they take control of Invested Businesses. However there are no published formal ROCE targets - management guidance focuses on PBT margin (>15% by 2029) and revenue growth (doubling by 2029).

Industry Structure & Competition

The UK mortgage market is large and the advice sector fragmented, with annual gross lending of £250–300bn in normalised conditions. The intermediary channel now accounts for over 80% of new mortgage originations, having grown structurally from ~50% in the early 2000s. Product complexity across 200+ active lenders has made broker-intermediated mortgages the default for most borrowers. MAB clearly see themselves as a hybrid of an AR network and a digital broker as shown below :

Other major networks or adviser groups of note would include Sesame Bankhall , Openwork, Connells/ Countrywide whilst major lenders such as Halifax also have dedicated intermediary channels.

In terms of competitive advantage for MAB I would highlight the following key aspects :

• MIDAS technology platform: Proprietary adviser management system providing compliance support, lender criteria search, Green Mortgage tools, and increasingly AI-driven case management. The data asset embedded in MIDAS — decades of transactional and behavioural data — underpins the AI strategy and is hard to replicate quickly.

• Brand & industry awards: MAB has won over 250 national industry awards for advice quality. In a trust-sensitive, regulated market, brand recognition and award track record reduce adviser acquisition costs and support client retention.

• Scale on lender panel: 90+ lender relationships with scale-based procuration fee rates that smaller networks cannot access. Superior fee terms improve both consumer outcomes (more choice) and network economics (higher procuration per case).

Cashflow, Balance Sheet & Capital Allocation

Balance sheet: Net debt £3.3m, reduced from £9.7m in FY2024. Surplus regulatory capital of £57m provides significant financial flexibility for further IB acquisitions without needing to access debt markets. Net tangible assets are modest — the balance sheet principally reflects goodwill and intangibles from acquired businesses — but this is structurally appropriate for an asset-light intermediary where the economic value resides in adviser relationships and technology.

Cash flow: Free cash flow of £36m in FY2025, 121% cash conversion. Operating cash generation is structurally high given minimal working capital requirements and low capex intensity. M&A cash deployment of £10m in FY2025 was mainly buying in minorities- all sensible housekeeping and consistent with expanding the IBs. In addition around £10m was invested across the business as part of the MAB 2.0 strategy.

Dividends : 22.5p paid in FY2025 – this was cut from 28.2p in FY2024 , increasing cover to 2x and was framed as a deliberate capital retention decision to fund M&A and invest heavily in the MAB 2.0 strategy. Despite this the shares still yield over 4% today and the DPS should grow strongly with EPS as they execute the 5 year plan.

M&A strategy: MAB has historically held minority stakes in businesses and has been tidying this up considerably in recent years, assuming full control of a number of them, most notably Dashly in 2025. I would expect this to continue with the Fluent minority likely to be bought in the next few years.

Management, Governance & Shareholders

Management

• Peter Brodnicki (co-founder, CEO since 2001) is one of the longest-serving CEOs in UK financial services. The MAB 2.0 framework feels like a defining strategic initiative and with 18% of the company he has huge skin in the game. However, succession planning will become a concern eventually and the key man risk for MAB is high given his tenure.

• Emilie McCarthy, CFO was appointed in 2024 and has built up good credibility with investors so far IMO.

• Yaiza Luengo, Chief Operating Officer: A new addition to the executive team. Oversees technology platform investment, IB integration, and adviser productivity initiatives — the operational core of the MAB 2.0 delivery.

Incentives & Governance

• Incentive alignment: Management incentives are structured around adjusted EPS growth and TSR — broadly appropriate. The FY2025 dividend reduction to retain M&A capital suggests management’s personal incentives are aligned with long-term value creation over short-term distributions.

Key Shareholders

Management holdings – as above. CEO / founder owns 18% and is crucial to future success.

The move from AIM to Main is set to complete by end April and has been a drag on the share price of late. Having had around 10% held by AIM IHT funds at the final results I believe this overhang has now largely been cleared, with Octopus recently selling most of their holding. Aberdeen have also reduced their stake materially whilst Liontrust continue to grapple with fund outflows.

It will be interesting to see if any material, new shareholders come on board once the move to the main market completes. MAB themselves expect to see an increase in overseas holders as a result.

Technicals & Momentum

The shares have been under pressure since hitting 800p in January, reflecting macro concerns about the UK housing market outlook (which has deteriorated in recent weeks) and the transition of the shareholder base from AIM to main. As such the technicals are weak with the shares below the 50 and 200d MA

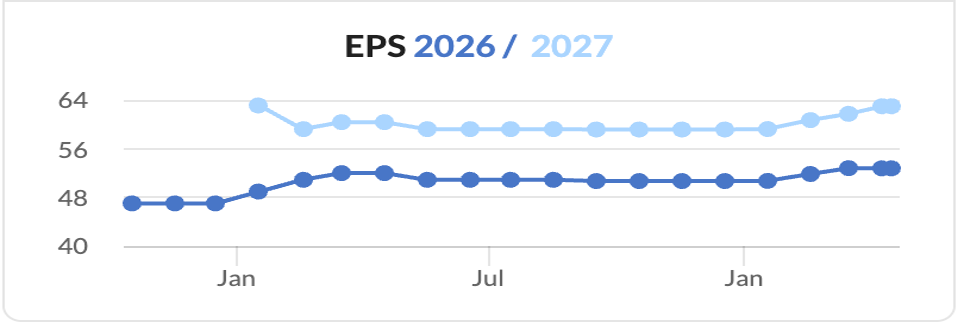

Earnings Momentum

Despite the recent weakness in the shares the EPS forecast trend has been one of solid improvement over the past year as the MAB 2.0 targets were set. Analyst coverage is reasonable with 4 brokers active – price targets range from 1000p to 1150p – suggesting strong potential upside from current levels (see valuation section below)

Guidance & Targets

• Management has set out a phased roadmap: full-year IB impact in 2026, admin centralisation in 2027, AI/tech case management in 2028, platform optimisation in 2029.

• FY2026 trading: Management reaffirmed MAB 2.0 targets above at FY2025 results. No specific FY2026 revenue guidance provided, but the IB admin cost ratio is expected to peak in FY2026 as FY2025 M&A acquisitions annualise — a key signpost for margin progression. Consensus PBT of £44m , a 20% uplift.

Bull & Bear Drivers (1–2 Year View)

Key Risks

• Mortgage volume cyclicality: MAB’s economics are directly tied to UK mortgage completion volumes. A sustained period of elevated UK rates, housing market stagnation, or a recession-driven collapse in transactions would materially impact revenue. The rate sensitivity is asymmetric — a 25bps rate increase can deter movers whilst rate cuts generate a lagged but positive volume response. FY2025’s 20% revenue growth was partly a recovery from the 2022–2023 rate shock trough and may not be fully repeatable in a normalised environment.

• MAB 2.0 execution risk: Revenue doubling + margin expansion + market share doubling by 2029 is ambitious. Management has a strong execution track record across economic cycles, but this is a more complex strategic programme than previous phases.

• Key person risk: Brodnicki has been CEO since 2001; principal relationship holder with major estate agency partners, lenders, and investors. His departure or incapacity would be disruptive, particularly during the critical MAB 2.0 execution phase. Succession planning is unaddressed as far as I am aware.

Upside Catalysts

• Product transfer market share acceleration : MAB holds just 3.0% of the £261bn product transfer market vs. 8.4% of new lending. As the wave of 5-year fixed rate mortgages originated at 2019–2022 lows matures through 2025–2027, the short term opportunity is there. Sustained evidence of share gains would be the most powerful re-rating catalyst.

• Margin expansion confirmation: FY2026 results demonstrating that IB admin costs have peaked and group PBT margin has moved above 12% toward 13–14% would provide direct evidence that the MAB 2.0 margin pathway is on track — likely triggering consensus upgrades and multiple expansion.

• Adviser count reaching 2,300+: Every 100 advisers at the current average revenue per adviser (~£157k) adds ~£15.7m of incremental annual revenue. Confirmation of continued double-digit adviser count growth would compound the revenue re-rating.

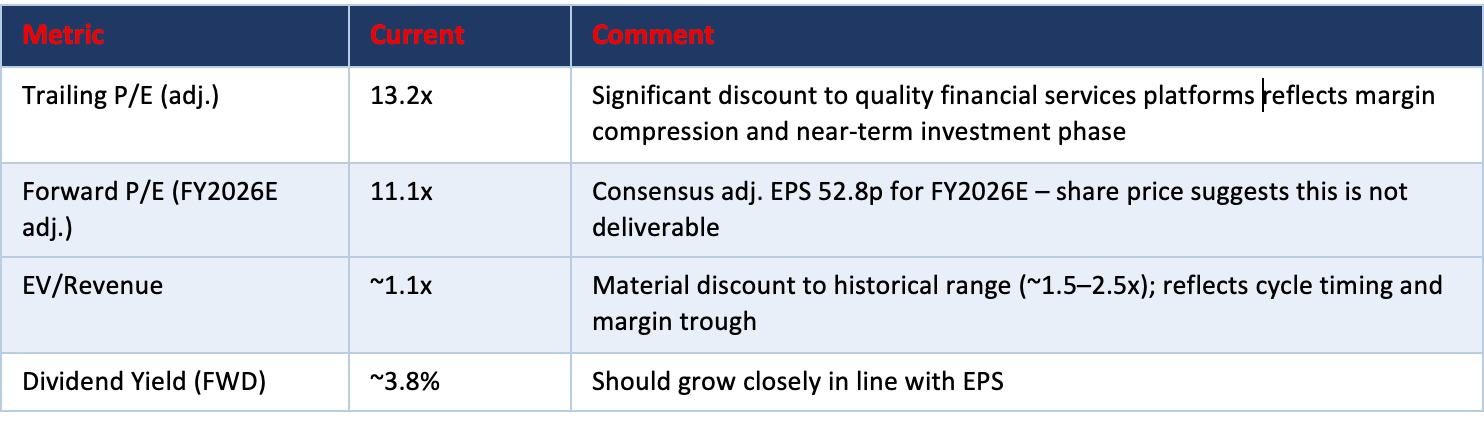

Valuation Framework

Current Valuation

What Is the Market Pricing In ?

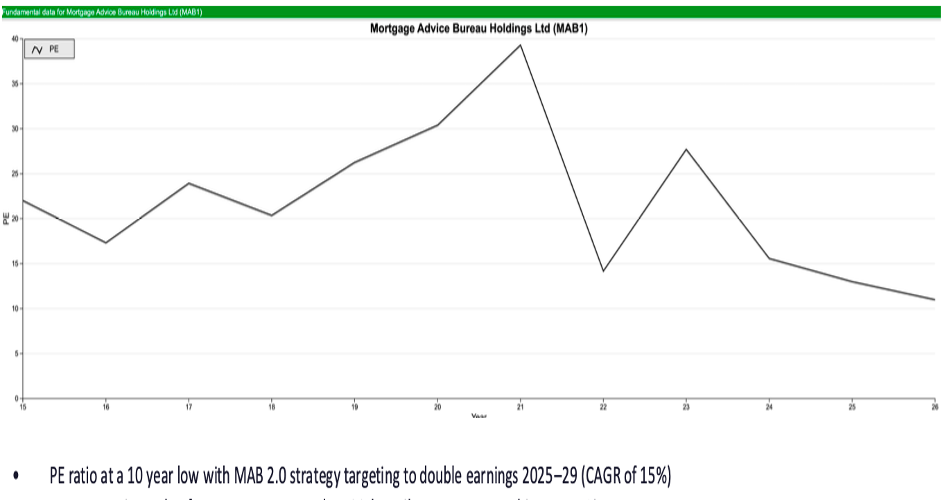

At current prices the market appears to be pricing MAB as a cyclical business— exposed to UK housing volumes and rate sensitivity — rather than as a compounding platform business executing a credible multi-year growth strategy. IMO the market is effectively pricing a high probability of MAB 2.0 failure or sustained margin compression, despite strong revenue and profit growth in FY2025.

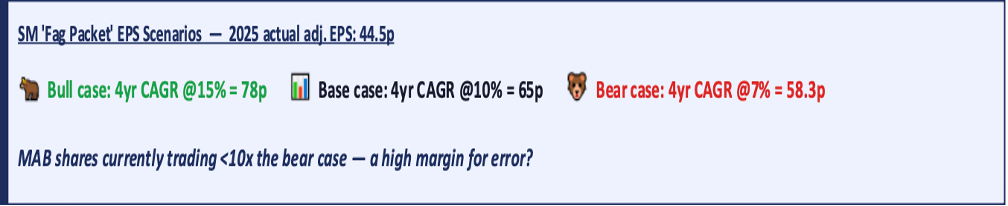

My best guess is that investors probably expect a CAGR in EPS of 5-7% versus the 15% implied by the 5 year plan.

Conclusion

The investment case for Mortgage Advice Bureau hinges on whether or not you believe that MAB is a growth company or merely a cyclical one, buffeted by the ups and downs of a UK mortgage market which is both mature and volatile. The MAB 2.0 strategy is bold and ambitious, targeting a doubling of the business by 2029. 2025 was a year of strong progress towards this target and management expect 2026 to deliver material profit growth too. The stockmarket is sceptical and values the shares at a multi year low. The upcoming move to the Main List from AIM whilst not a catalyst in itself should at least remove a heavy burden on the shares, allowing investors to reappraise the business whilst the valuation is low today.

To get anywhere near the medium term targets there are two key things to achieve.

1) Materially higher profit margins – driven by increased volume / scale, productivity gains and growth in invested businesses

2) Materially higher market share – driven by digitalization , increased penetration in product transfers and a multi channel market approach with lead generation at it’s core.

Mortgage Advice Bureau is a structurally sound business with a 25-year operating track record, a 34% ROCE , strong FCF conversion, and a credible pathway to doubling in size by 2029. For most of it’s history the track record has been excellent and the business has prospered despite multiple economic shocks, all of which suggests to me they are well equipped for an uncertain future …. whilst trading at a material valuation discount. Time to visit the bureau de change.